Autumn 2022 Update on UK’s Project Gigabit Broadband Rollout

The Building Digital UK team has published their latest quarterly Winter 2022 update for the Government’s £5bn Project Gigabit broadband rollout scheme, which summarises some good progress, but also reveals that procurements for Lancashire, Surrey and Oxfordshire and West Berkshire have had to be deferred.

Just to recap. Project Gigabit aims to extend networks capable of delivering 1000Mbps (1Gbps) download speeds to “at least” 85% of UK premises by the end of 2025 and then “nationwide” coverage (c.99%) by around 2030 (here). The funding released for this will depend upon how the industry responds. So far only £1.2bn has been released from the budget up until 2024, but more is expected to be unlocked later.

At present around 72% of UK premises can already access a gigabit-capable network (c.42% via just FTTP) and that’s mostly thanks to Virgin Media’s (VMO2) upgrade of their existing HFC networks (here). Generally, it’s anticipated that commercial builds alone could push gigabit coverage up to a little over 80% by around the end of 2025 (mostly in urban areas).

Advertisement

Project Gigabit is thus designed to focus on improving connectivity for those rural and semi-rural areas in the final 20% (5-6 million premises). This consists of several support schemes, including gigabit vouchers (£210m), funding to extend Dark Fibre around the public sector (£110m) and gap-funded deployments with suppliers (rest of the funding) – better known as the Gigabit Infrastructure Subsidy (GIS) programme.

Today’s article is focused upon the GIS programme and related procurement work, which sees ISPs bidding through a new Dynamic Purchasing System (DPS) to extend their networks across disadvantaged parts of the UK.

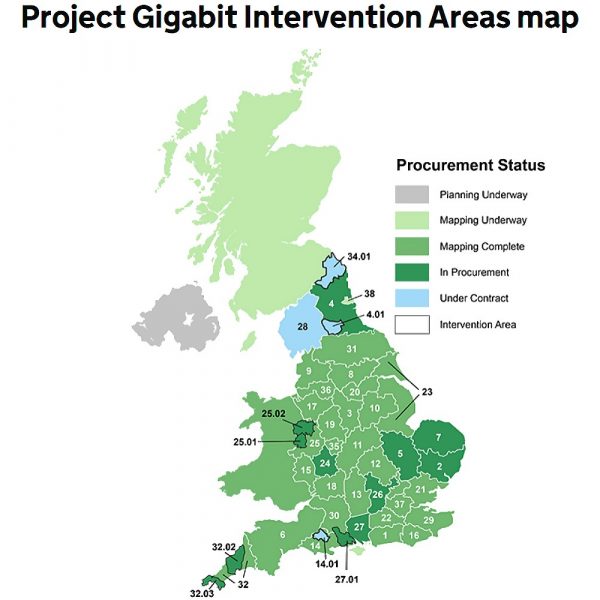

What’s New in the Autumn 2022 Update

Since the last update, BDUK has followed their initial contract award for North Dorset (Lot 14.01) (here) by adding several more for Teesdale (Lot 4.01 –here), North Northumberland (Lot 34.01 – here) and Cumbria (Lot 28 – here) – reflecting a combined value of more than £128m in public investment to upgrade nearly 75,000 premises (c.£1,700 per premises passed).

As it stands, the total value of Project Gigabit’s procurements launched to date is over £780 million, which if successfully delivered would see up to 545,000 extra premises being passed by a gigabit-capable network. But so far all of this has been in England, while the devolved countries of Wales, Scotland and Northern Ireland are still in the preparation stage (Wales is further along, so we expect some updates next spring).

Advertisement

However, it’s not all good news. At the last update we noted that BDUK had opted to defer the procurements in Shropshire (Lot 25), Staffordshire (Lot 19) and the eastern part of Hertfordshire (part of Lot 26) due to a fear – post engagement with suppliers – that they “will not be successful” (i.e. suppliers showed limited interest). Now the same can also be said for Lancashire (Lot 9), Surrey (Lot 22) and Oxfordshire and West Berkshire (Lot 13).

The BDUK team will be working to find a solution for those on the deferred procurements list, which we suspect could require changes to the cluster sizes they cover or perhaps splitting them into several smaller local supplier procurements. But for now, those procurements are all in limbo and marked TBC on the list.

Live GIS Contracts (Signed)

| Area | Contract Awarded | Uncommercial Premises | Value |

|---|---|---|---|

| North Dorset (Lot 14.01) | 25-Aug-22 | 7,100 | £6.3 million |

| Teesdale (Lot 4.01) | 22-Sep-22 | 4,100 | £6.6 million |

| North Northumberland (Lot 34.01) | 14-Oct-22 | 3,790 | £7.3 million |

| Cumbria (Lot 28 | 29-Nov-22 | 59,000 | £108.5 million |

Take note that, once a contract has been signed, it often takes network operators several months of engineering surveys before they can begin to start a rollout. Likewise, the detailed rollout plan for these first contracts won’t be known until those surveys have been completed. Furthermore, the contract values above are only referencing public investment, but it’s hoped that suppliers may also contribute some of their own private investment.

Advertisement

On top of the already agreed contracts, Project Gigabit also has a growing number of local and regional deals in the procurement phase for other parts of the UK (see below) and will be awarding contracts for these over the coming months and years. The dates and figures mentioned below are tentative estimates (subject to change) and will remain that way until after the contracts have been awarded.

Bidders on the related LOTS will be required to ensure that their networks and infrastructure are available for use by other ISPs via wholesale (open access). Various operators, both big and small (e.g. Openreach, Cityfibre, Fibrus, Gigaclear, Virgin Media [VMO2] etc.), are expected to take part and areas with sub-30Mbps speeds are being prioritised, albeit NOT to the exclusion of all else.

Alongside all this, the government and local bodies are also conducting various Public Reviews and Open Market Reviews (OMR), which is the process they use when trying to identify existing commercial coverage of gigabit-capable networks and any planned coverage over the next c.3 years. By doing that, they can more easily target their support toward areas where commercial projects will not go (i.e. the intervention area).

Live GIS Procurements

| Area | Est. Contract Award Date | Uncommercial Premises | Value |

|---|---|---|---|

| Central Cornwall (Lot 32.03) | Jan-23 | 9,750 | £18 million |

| South West Cornwall (Lot 32.02) | Jan-23 | 9,500 | £18 million |

| New Forest (Lot 27.01) | April to June 2023 | 10,500 | £14.5 million |

| Mid West Shropshire (Lot 25.01) | April to June 2023 | 7,300 | £10.8 million |

| North Shropshire (Lot 25.02) | April to June 2023 | 12,200 | £24 million |

| North East England (Lot 4) | April to May 2023 | 53,250 | £82.7 million |

| Cambridgeshire and adjacent areas (Lot 5) | Feb-23 | 49,700 | £68.6 million |

| Norfolk (Lot 7) | Mar-23 | 86,200 | £114.2 million |

| Suffolk (Lot 2) | Mar-23 | 87,200 | £100.4 million |

| Hampshire (Lot 27 | April to June 2023 | 88,600 | £104.1 million |

| Worcestershire (Lot 24) | July to September 2023 | 18,460 | £39.4 million |

| Buckinghamshire, (part of) Hertfordshire and East of Berkshire (Lot 26) | July to September 2023 | 40, 320 | £58.7 million |

Finally, BDUK has a long list of future procurements in their pipeline (see below). But some projects (e.g. Scotland and Wales) haven’t even got this far yet. The following pipeline thus represents an indicative forward view of commercial activity to be undertaken by the programme. Some of the information provided is based on modelled data that will be superseded.

Future GIS Procurements

| Area | Est. Contract Award Date | Uncommercial Premises | Value |

|---|---|---|---|

| Kent (Lot 29) | July to September 2023 | 72,000 | £112 million |

| East and West Sussex (Lots 16 and 1) | July to September 2023 | 62,100 | £100 million |

| Bedfordshire, Northamptonshire and Milton Keynes (Lot 12) | October to December 2023 | 46,700 | £60 million |

| Derbyshire (Lot 3) | October to December 2023 | 36,210 | £53 million |

| Wiltshire and South Gloucestershire (Lot 30) | October to December 2023 | 84,800 | £85 to 145 million |

| Leicestershire and Warwickshire (Lot 11) | November 2023 to January 2024 | 72,200 | £90 million |

| Nottinghamshire and West of Lincolnshire (Lot 10) | November 2023 to January 2024 | 46,900 | £63 million |

| West Yorkshire and parts of North Yorkshire (Lot 8) | November 2023 to January 2024 | 45,990 | £68 million |

| South Yorkshire (Lot 20) | November 2023 to January 2024 | 51,780 | £55 million |

| Lancashire (Lot 9) | TBC | 31,000 | £55 million |

| Surrey (Lot 22)* | TBC | 99,400 | £101 to 171 million |

| Shropshire (Lot 25)* | TBC | 20,700 | £30 to 40 million |

| Staffordshire (Lot 19)* | TBC | 70, 800 | £72 to 123 million |

| Oxfordshire and West Berkshire (Lot 13)* | TBC | 18,500 | £32 million |

| Cheshire (Lot 17) | January to March 2024 | 74,300 | £85 to 144 million |

| Devon and Somerset (Lot 6) | January to March 2024 | 159, 600 | £198 to 337 million |

| Herefordshire (Lot 15) | January to March 2024 | 23,700 | £30 to 60 million |

| Gloucestershire (Lot 18) | January to March 2024 | 44,700 | £40 to 80 million |

| Lincolnshire (including NE Lincolnshire and N Lincolnshire) and East Riding (Lot 23) | January to March 2024 | 105, 700 | £106 to 180 million |

| Dorset (Lot 14) | April to June 2024 | 56,500 | £62 to 105 million |

| Essex (Lot 21) | April to June 2024 | 78, 400 | £79 to 135 million |

| Northern North Yorkshire (Lot 31) | April to June 2024 | 28,200 | £25 to 42 million |

| Birmingham and the Black Country (Lot 35) | April to June 2024 | TBC | TBC |

| Merseyside and Greater Manchester (Lot 36) | April to June 2024 | TBC | TBC |

| Greater London (Lot 37) | April to June 2024 | TBC | TBC |

| Newcastle and North Tyneside (Lot 38) | April to June 2024 | TBC | TBC |

Michelle Donelan MP, UK Digital Secretary, said:

“Our country has faced-down and overcome some enormous challenges in recent years, all of which have shown the potential for us to genuinely go further and faster than anyone imagined in order to make people’s lives tangibly better. At the Department for Digital, Culture, Media & Sport, I am determined to ensure we continue to deliver at speed for the British people.

This is absolutely the case at Building Digital UK (BDUK). Over the past few months, multi-million pound local and regional Project Gigabit contracts have been awarded that will result in major improvements for people living in rural or otherwise hard-to-reach areas of the United Kingdom. Businesses will be boosted, job opportunities broadened, life chances enhanced.”

At present it’s disappointing to see that BDUK still hasn’t managed to launch a centralised website for clearly communicating their progress on each contract / area. The quarterly updates they issue are useful to sites like ours and the media, but they’re simply too tedious for regular people to find, read and understand, unless you’re already familiar with the programme.

The other issue is that it continues to take far too long to get all of these contracts into procurement. The new and more automated DPS system was supposed to make all of this faster and more efficient than just handing the funding to local authorities, but with some areas being left until 2024 or 2025 before contracts are even awarded, it may be time to start questioning whether this is the right approach.

We should remind readers that this rollout is NOT an automatic upgrade, thus you will still need to order the service from a supporting ISP (1Gbps is the target speed, but slower and cheaper options will also exist). Likewise, no specific network coverage checkers will be available for areas in this programme, at least not until AFTER the contracts have been awarded and the necessary engineering surveys are completed.

The focus on “gigabit” speeds also overlooks the fact that this largely relates to download performance, while BDUK’s technical definition for the project appears to suggest that a minimum speed of 200Mbps would be acceptable when only looking at the upload side (here). This is understandable, as not all gigabit networks today are actually setup to deliver true symmetric gigabit speeds, even though some may advertise them.

Lest we forget that there are a lot of real-world reasons why consumers buying a 1Gbps package might not actually be able to achieve the top speed, due to certain realities (Why Buying Gigabit Broadband Doesn’t Always Deliver 1Gbps).

Finally, we should add that the Government has previously warned that those in the final 1% may still be “prohibitively expensive to reach“, although they’ve recently clarified that less than 0.3% of the country (i.e. under 100,000 premises) are likely to fall into this category (roughly the same gap that the 10Mbps USO has struggled to fill). Solutions for those in the final 0.3% of “Very Hard to Reach” areas are still being tested.

Project Gigabit Autumn 2022 Update

https://www.gov.uk/../project-gigabit-delivery-plan-autumn-update-2022

Mark is a professional technology writer, IT consultant and computer engineer from Dorset (England), he also founded ISPreview in 1999 and enjoys analysing the latest telecoms and broadband developments. Find me on X (Twitter), Mastodon, Facebook, BlueSky, Threads.net and Linkedin.

Nice to see they have admitted the North East England Lot 4 Procurement has slipped by appx. 8 months maybe longer.

Looking at the original data it was clear to anyone with eyes in their head that Gigabit was already available in large parts of the intervention areas. I thought that was the whole point of the Open Market Reviews, these things don’t happen overnight and are years in the planning so they should have known.

Nothing from DCMS on this until this update, and no actual data to look at to see the revised intervention areas – I guess until the procurement is relaunched in Jan 23.

The 2025 can just keeps on getting kicked down the road.

The OMR are partially good and partially a mess. Hampshire for instance had mapped much of that was already needed.

We have a cbt outside our house, ready to be plugged into a splitter and lit. Its been there for two years.A combination of legal woes and funding has stalled it. It got chucked into project gigabit. I’m now expecting april/june for the work to be complete..

This is one example of how omr has failed.

If 200Mbps upload is a requirement to count as gigabit, why does any of Virgin Media’s network count? Highest upload speeds are a paltry 50Mbps even on Gig1

The article does say it appears to suggest and isn’t a concrete set out definition. Virgin really should allocate some more of their bandwidth towards upload. 5% is not enough. It hopefully shouldn’t matter too much for that much longer as they do have plans to convert everyone on their network to FTTP by 2028.

Virgin’s uplink speeds are a joke.

November 2023 – January 2024

Nice to have some kind of estimation rather than a generic and vague “by 2026.”

Hopefully it’s FTTP and not 5G.

Contract award date? Is that the time period where spades are intended to be in the ground and FTTP is being installed to addresses in that area?

AFAIK, it’s exactly what it says. It’s when the contract gets awarded. Build could be easily another 18 months or so. Our area is contract award Q1 2024, and Openreach plan FTTP by end 2026. Airband were awarded a major contract nearly two years ago, and they are still building…

Are they significantly behind on the contract awards? Hampshire looks way delayed!

Another Starlink trial: https://www.bbc.co.uk/news/technology-63819322

As someone waiting on the outcome of Lot 4, I continue to not hold my breath, and invest in 4G/5G kit.

Anything for South Wales? It seems when they talk Rural they don’t mean places like Tylorstown in the Rhondda Valleys…..

I was told a couple of days ago that a number of houses had FTTP but they failed to tell me why they had stopped, other than a lame excuse that because the rest of the houses were back fed not front, plus installing Fibre on the poles either the OR engineer was talking out of a orifice or its still way off? I dread to think how much I’d be quoted for a FTTP connection to be installed?

I sense is going to be beyond 2027 before we get FTTP if at all?

It’s the same story in Abertillery, Blaenau Gwent no sign of it being rolled out here either.

Let’s hope North Norfolk gets some FTTP loving as my FTTC speeds are degrading as 300+ users are on the same cabinet as me.