INCA – Alternative Full Fibre Broadband Networks Cover 19.7 Million UK Premises

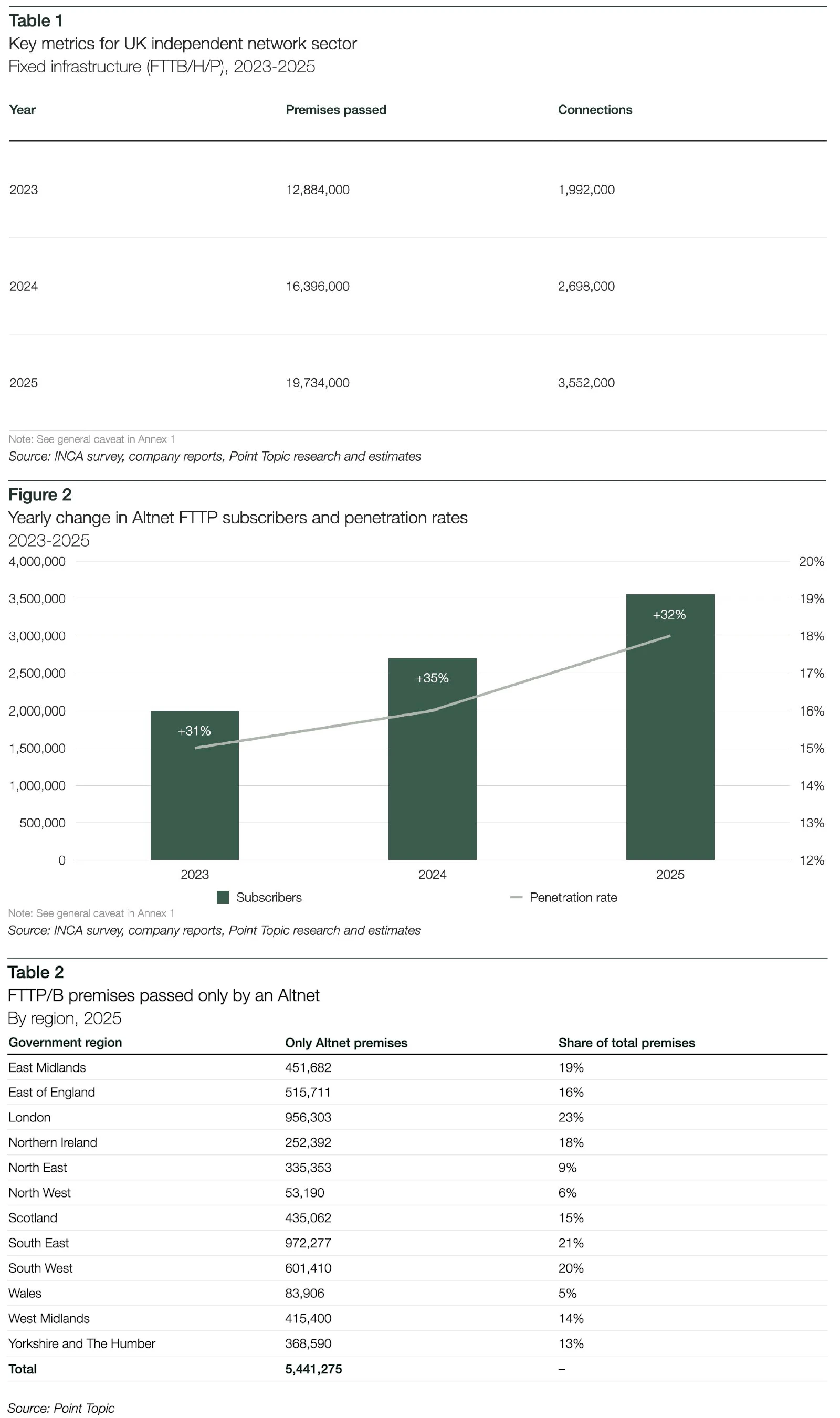

The Independent Networks Co-operative Association (INCA) and Point Topic have today released their 2026 report into the impact of alternative “full fibre” (FTTP/B) broadband networks in the UK. The study reveals that their coverage grew by 20% in 2025 to top 19.7 million premises (up from 16.4m or 27% in 2024) and there are more than 3.5 million live connections (up by 32%).

Just to be clear on something. INCA’s study excludes Fibre-to-the-Premises (FTTP) deployments from the two largest operators – Openreach (BT) and Virgin Media (VMO2) – in order to focus on independent Altnets like CityFibre, Netomnia, Gigaclear, Hyperoptic, CommunityFibre and many more (Summary of UK Full Fibre Builds).

The report reveals that Altnets now cover a total of over 19.7m premises ready for service, which is up by 20.1% from 16.4m last year, but with coverage growth clearly slowing from 27% in 2024. Furthermore, some 4.4m of those were in places classed by Ofcom as “Area 3” (i.e. mostly harder to reach rural locations), which is up 20% from 3m last year and means that Altnets have delivered full fibre to 46% of UK premises in harder to reach rural areas.

Advertisement

Take-up also stands at 18% (3.5 million live connections), which is up from 16.5% last year (2.7 million live connections) – an annual growth rate of 32% (down from 35% last year). But the fact that there’s been a slowdown in altnet coverage won’t come as much of a surprise to ISPreview’s readers, as it reflects the wider economic strains (rising build costs, competition and high interest rates), with many altnets having cut jobs and slowed their build over the past 2-3 years in order to focus on greater commercialisation.

Overall, there’s still a fair bit of build activity in the altnet space and a lot more to come, but the 2025 period was clearly another challenging one like the year before.

One possible caveat above is that there can be a tendency for some network operators to report technically unfinished or non-live builds (i.e. you can’t yet order a live service) as Ready for Service (RFS), which may cause complications when forecasting live coverage.

Advertisement

The Financial Impacts

According to INCA, investment in the Altnet sector significantly improved during 2025, with an estimated £3.2bn of additional funding being committed to network expansions (up from £574m last year). But to be fair most of that did come from a handful of providers, including CityFibre’s July 2025 announcement of £2.3bn in funding from a private investment consortium.

However, we should point out that aspirational funding commitments are subject to significant change, much like the builds themselves, and thus should be viewed with caution. Some projects will fail, reduce or be consolidated, so we don’t expect all of this to always be fully realised (accurately accounting for this is extremely difficult due to the lack of transparency from some operators).

However, taking this private sector investment together with the government’s £5bn Project Gigabit commitment (there’s less than £2bn available from that budget), as well as other planned full fibre investments (e.g. £15bn from Openreach’s FTTP deployment), quickly highlights just how much investment is still flowing into the market. The vast majority of that is still private funding, which takes a lot of the strain away from the public purse.

Advertisement

Additional INCA Findings

- Altnets have expanded their full fibre footprints by 35% over the three-year period between 2023-2025

- Openreach’s markets share has declined by around 2%, indicating that Altnets are not only capturing displaced demand from incumbent networks, including Virgin Media O2 (whose penetration rates declined by 3.4 percentage points between 2023-25), but are doing so at scale

- Altnets entry-level pricing in 2025 stood at £19, down from £22 in 2020. National providers are currently significantly higher – BT (£35); Sky (£25); and TalkTalk (£25).

- Over the 5-year period, Altnets average price was broadly stable (£39 in 2020 v £38 in 2025) – this compared to notable reductions in the average prices from BT (£46 to £40); and Virgin Media O2 (£49 to £34). This data strongly suggests that intensified Altnet network competition has been driving downward pressure on mainstream pricing.

- The top 20 ISPs ranked by consumers on Trust Pilot are Altnets, with none of the four major retail ISPs appearing in this list. On average independent ISPs achieve a rating of 4.4 out of 5 compared with BT (1.3), Sky (1.8), TalkTalk (2) and Virgin Media O2 (2.4)

- Yorkshire and Humberside has the largest Altnet coverage, with at least 60% of premises able to access FTTP from an Altnet

Findings from the consumer study included:

- 76% of Altnet customers agreed that “my broadband provider offers good value for money”, compared to 68% of major providers; and 33% of Altnet customers compared to only 19% of major provider customers said they “strongly agree” with this.

- 1 in 10 users of national broadband providers are considering switching to smaller/independent providers, representing around 2.5 million households

- 41% of users of national broadband providers feel or expect that smaller providers care more about their customers, whereas 65% of Altnet users had the same thoughts – and Altnet customers are twice as likely to say ‘strongly’ so (by 20% to 9%)

- Altnet customers are more likely to trust their broadband provider to act in their best interests as a customer, and “strongly” so, by 25% to 19%

- More users of national broadband providers (70%) worry about hidden costs or unexpected price rises than Altnet users (60%)

- More users of national broadband providers (65%) feel that broadband is more complicated than it needs to be compared with Altnet users (58%)

- One in three Altnet customers agree “strongly” that they are “satisfied with the customer service I receive from my current broadband provider” compared to one in four national broadband provider customers

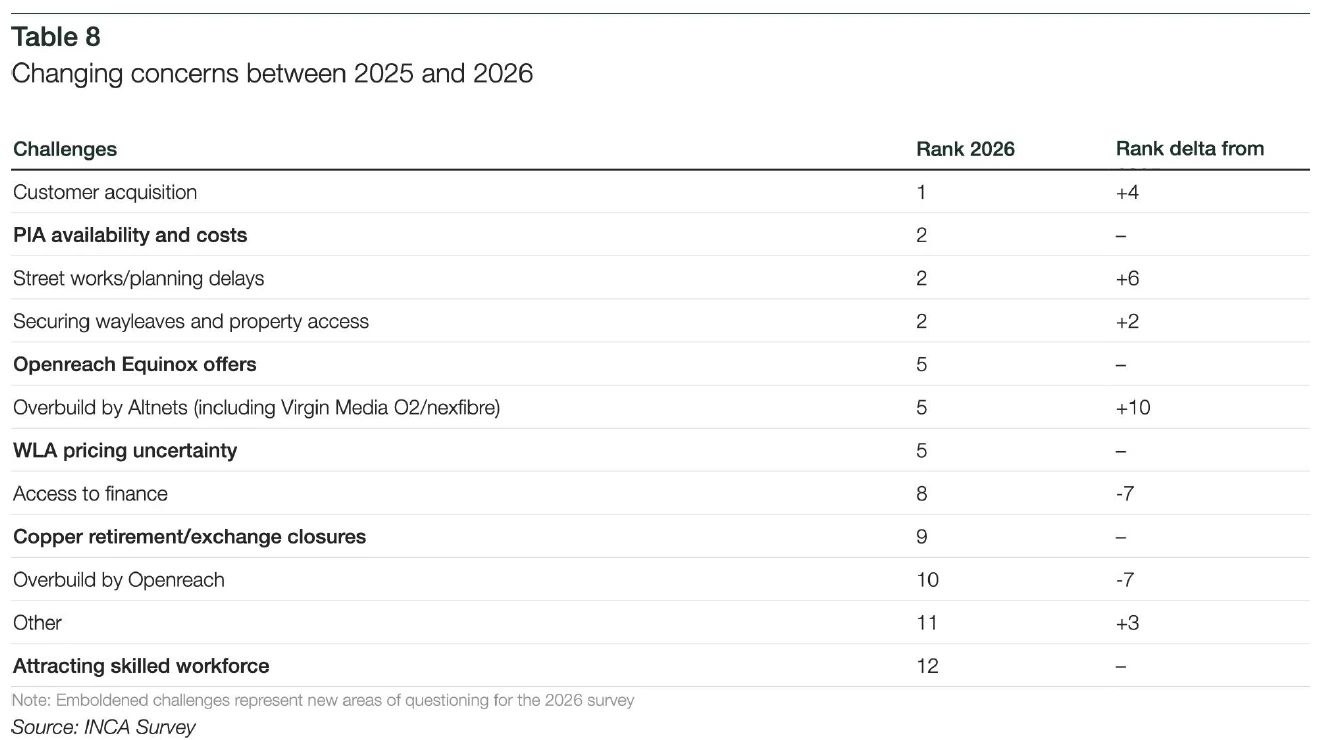

The Most Pressing Issues for Altnets

Finally, in terms of the issues that AltNets think are the most pressing to tackle, it’s worth looking back at last year’s report to see what the top concerns were during 2025. According to last year’s report, the top concerns were – 1) Access to finance, 2) Switching between Openreach and independent networks e.g. through the One Touch Switching process, and, 3) Getting wayleaves.

By comparison, the top concerns in this year’s report are – 1) Customer acquisition, 2) PIA availability and costs (i.e. access to run fibre via Openreach’s existing cable ducts and poles), 3) Street works/planning delays, and 4) Securing wayleaves and property access. Numbers 2, 3 and 4 all tied in second place.

Overall, Altnets are continuing to have a significant impact across the United Kingdom and that is set to continue for the foreseeable future, which is one of the reasons why major network operators are ramping-up their own builds (competition). But at the same time, there’s likely to be more consolidation in the market over the coming year as financial strains continue to bite.

The recent deal between VMO2’s parents and Netomnia suggest a direction that could also make it harder for a third major infrastructure provider to build toward a truly competitive scale, with one risk being that we could end up back with a duopoly of Openreach and Virgin Media, alongside a bunch of smaller-scale players. Time will tell.

Paddy Paddison, CEO of INCA, said:

“Whilst there is much work to do by the independent network sector and still a lot to play for, the data from both studies shows real promise for Altnets.

There is definitely a ‘changing of the guard’ emerging in the broadband marketplace. Altnets are pretty much matching the big players for new connections growth, taking share from them, and there is a lot of evidence that the independent market is giving the big providers more than a run for their money when it comes to customer value and experience. That is vindication for the Government’s policies to create more competition in the ultrafast broadband market – and the UK is now benefitting from it.

We’re now seeing Altnets moving from supplementing incumbent networks to increasingly being the primary source of full fibre connectivity for millions of households.”

It is also worth noting that Altnets have the more complex task of winning new customers onto their network, as opposed to the incumbents who can convert existing customers onto their full fibre services. On the flip side, between 2024 and 2025, Openreach reported approximately 860,000 net line losses, which is closely mirrored by around 850,000 net additions by Altnets over the same period.

INCA State of the Altnets 2026 Report

https://inca.coop/state-of-the-altnets-2026/

Mark is a professional technology writer, IT consultant and computer engineer from Dorset (England), he also founded ISPreview in 1999 and enjoys analysing the latest telecoms and broadband developments. Find me on X (Twitter), Mastodon, Facebook, BlueSky, Threads.net and Linkedin.

« Broadband ISP EE UK Make DAZN App Available to Pay TV Customers

Is the report publicly available?

Knew I forgot something 🙂 . See new link at the bottom of the article.

“but with coverage growth clearly slowing from 27% in 2024”

2023-24: 12.884m to 16.396m = 3.512m added

2024-25: 16.396m to 19.734m = 3.338m added

That’s only 5% down, and is pretty good considering that much of the cherry picking has already been done.

they only represent a few and they don’t do much, in truth it can deceive the total amount of alt net coverage

Does INCA consider nexfibre to be altnet or part of Virgin Media for the purposes of these figures?

The 19m figure presumably includes colossal overlaps between INCA members (my address would be one of them. I would assume it is double counted). 5.4m covered outside of Openreach’s current footprint is impressive, though likely massively taxpayer subsidised.

Still, it’s nice to see an INCA report that doesn’t deliberately use the term “BT Openreach”. Amusing to see that PIA concerns are number 2 – maybe if your business depends on the regulator forcing your primary competitor to be nice to you, it’s not a great model to begin with.

Interesting to use price as a talking point. What happens when they can’t fund it all on debt any more and have to attempt to pivot to financial sustainability?