BDUK Publish Phase 3 of UK Rural Gigabit Broadband Rollout Plan

The UK Government’s Building Digital UK (BDUK) team has today published details on Phase 3 of their £5bn Project Gigabit rollout programme, which will in this phase work to extend 1Gbps capable broadband ISP networks to a further 570,000 premises in rural and semi-rural areas.

In case anybody has forgotten, Project Gigabit seeks to extend such speeds to reach at least 85% of UK premises by the end of 2025 and “as close to 100% as possible.” The funding released for this will depend upon how the industry responds (i.e. so far only £1.2bn has been released, but more will be unlocked if the industry shows it can deliver).

At present nearly 60% of UK premises can already access a gigabit-capable network (c.27% via just FTTP), which should reach c.65% by the end of 2021 (here) and that’s mostly thanks to Virgin Media’s HFC upgrade. Generally, it’s hoped that commercial builds could push this up to around 80% by the end of 2025 (mostly in urban areas). But after that, private investment alone would struggle to go much further (rural builds become disproportionately expensive).

Advertisement

In short, Project Gigabit will step in to focus on improving connectivity to those rural and semi-rural areas in the final 20% (5-6 million premises). The project actually consists of several support schemes, including gigabit vouchers (£210m), funding to extend Dark Fibre around the public sector (£110m) and gap-funded deployments with suppliers (rest of the funding). In today’s article we’re focused on the latter, which sees ISPs bidding – via a new Dynamic Purchasing System (DPS) run by BDUK – to extend their networks across rural parts of the UK.

What’s in Phase 3

The first procurement phase (Phase 1a) of this project was announced in March 2021 and that covered parts of Cambridgeshire, Cornwall, Cumbria, Dorset, Durham, Essex, Northumberland, South Tyneside and Tees Valley. The next set of Phase 1b and Phase 2 procurements were then unveiled in August 2021 (here), which covered many more areas in England, stretching across a total of 26 counties.

So far, between Phases 1 and 2, Project Gigabit has already set out a procurement plan for helping to reach 2.2 million additional premises (mostly in England). Some 234,000 premises will also be tackled in Wales as part of the project (here).

By comparison, today’s Phase 3 announcement adds a further 570,000 premises to all that and this covers parts of Cheshire, Devon, Dorset, Somerset, Essex, Herefordshire, Gloucestershire, Lincolnshire, East Riding and North Yorkshire.

Advertisement

Nadine Dorries MP, UK Digital Secretary, said:

“The latest stage of our £5 billion Project Gigabit plan will help hard-to-reach homes and businesses out of the broadband slow lane and plug them into the fastest and most reliable connections available.

This investment is levelling up in action – building new internet connections in our rural communities so people have the speed, reliability and freedom to live and work flexibly, and take advantage of new technologies.”

As we’ve previously reported, the first contracts under Phases 1 and 2, once awarded (assuming no major delays), are expected to commence from May 2022. The very first rollout phase will include 349,000 premises across Essex, Dorset, Cumbria, Cambridgeshire, Northumberland, Durham, Tyneside, Teesside and Cornwall.

However, it often takes operators several months of engineering surveys before they can begin the rollout itself, which means building on the above may not start until toward the end of 2022. Naturally, with the plan for Phase 3 being unveiled later than Phases 1 and 2, the expected commencement date for related contracts is even later and will start between February and October 2023 (details below). As a result, the physical network build for much of Phase 3 won’t even begin until early 2024.

Bidders on the related LOTS will be required to ensure that their networks are available for use by other ISPs via wholesale (open access). Various operators, both big and small (e.g. Openreach, CityFibre, Gigaclear, Virgin Media [VMO2] etc.), are expected to take part and areas with sub-30Mbps speeds will be prioritised, albeit NOT to the exclusion of all else.

Alongside all this, the government and local bodies are conducting various Public Reviews and Open Market Reviews (OMR), which is the process they use when trying to identify existing commercial coverage of gigabit-capable networks and any planned coverage over the next c.3 years. By doing that, they can more easily target their support toward areas where commercial projects will not go (i.e. the intervention area).

Advertisement

Project Gigabit Phase 3 Areas

(Details below are estimated and subject to change)

| Procurement Start Date | Contract commencement date | Modelled number of uncommercial premises in the procurement area | Indicative Contract Value | |

| Dorset | May – Jul 2023 | Apr – Jun 2024 | 56,500 | £62 – £105m |

| Cheshire | Feb – Apr 2023 | Jan – Mar 2024 | 74,300 | £85m – £144m |

| Devon & Somerset | Feb – Apr 2023 | Jan – Mar 2024 | 159,600 | £198m – £337m |

| Herefordshire & Gloucestershire | Feb – Apr 2023 | Jan – Mar 2024 | 64,600 | £67m – £113m |

| Essex | May – Jul 2023 | Apr – Jun 2024 | 78,351 | £79m – £135m |

| Lincolnshire (including NE Lincolnshire and N Lincolnshire) and East Riding | May – Jul 2023 | Apr – Jun 2024 | 105,700 | £106m – £180m |

| Northern North Yorkshire | Aug – Oct 2023 | Jul – Sep 2024 | 28,200 | £25m – £42m |

We should remind readers that this rollout is NOT an automatic upgrade, thus you will still need to order the service from a supporting ISP (1Gbps is the target speed, but slower and cheaper options will also exist to order). Likewise, no specific network coverage checkers will be available for areas in this programme, at least not until AFTER the contracts have been awarded and the necessary engineering surveys completed.

Finally, we should add that the Government has previously warned that those in the final 1% may still be “prohibitively expensive to reach“, although they’ve recently clarified that less than 0.3% of the country (i.e. under 100,000 premises) are likely to fall into this category (roughly the same gap that the 10Mbps USO has struggled to fill). Solutions for those in the final 0.3% of “Very Hard to Reach” areas are currently being consulted upon.

We are expecting details of Scotland’s Project Gigabit rollout to follow soon.

Project Gigabit Autumn 2021 Update (PDF)

https://assets.publishing.service.gov.uk/../Project_Gigabit__Autumn_Update-complete.pdf

UPDATE 7:46am

We’ve noticed in this update that there have been a few changes to the previous Phase 1 / 2 plans, which largely reflects the fact that commercial deployments (e.g. Openreach’s plan to cover 25 million premises with FTTP by December 2026) are now expected to cover significantly more premises than previously envisaged.

As a result of the above, the amount of premises identified in their regional procurements have been reduced, although the subsidy required to deliver gigabit infrastructure has not been correspondingly reduced, since residual premises are the hardest to reach (i.e. the more rural you go, the higher the cost of build).

Key changes are as follows:

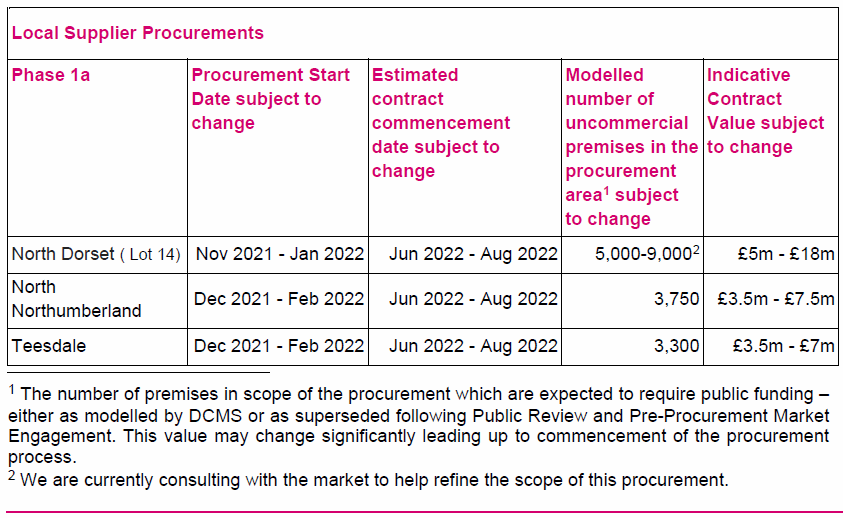

1. In Cumbria, the first of our Regional Supplier procurements, we have launched a procurement for 62,000 premises, down from 66,300, for up to £109m.

2. In Cambridgeshire, we now expect to procure 40,000 to 50,000 premises rather than our previously modelled estimate of 98,500.

3. In east Essex, the first area we targeted for a Local Supplier procurement, commercial plans were so extensive that there were only approximately 800 premises where we could justify intervention, compared to an original model estimate of 6,500. We believe targeted Gigabit Vouchers will provide a better solution than procurement in this case.

4. In Dorset, we have identified a potential Local Supplier procurement which combines two potential Local Supplier areas and will complement significant commercial plans for telecoms providers active in the area.

5. We are planning to combine Regional Supplier procurement areas in Northumberland and Durham, and have found two areas where we believe Local Supplier procurements will offer bidding opportunities to more telecoms providers.

UPDATE 8:10am

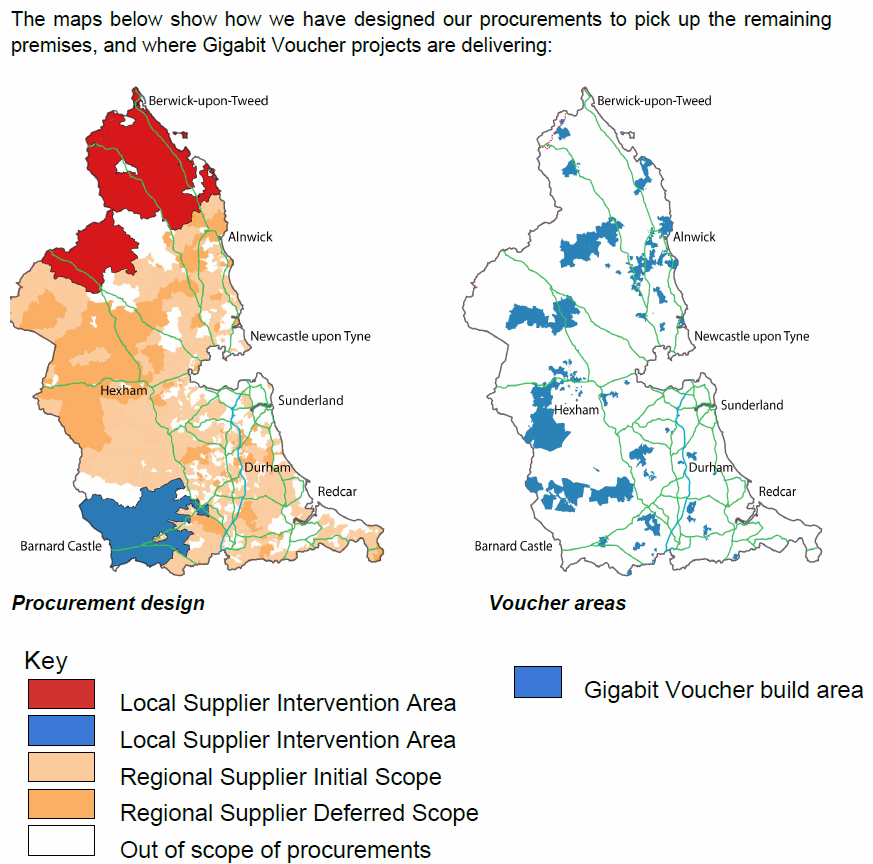

Aside from the larger Regional Supplier Contracts, the above changes also make reference to Local Supplier Contracts, which we haven’t talked about much before. Local supplier contracts are generally smaller, focus on the hardest to reach areas and intended to target slow spots in advance of the wider rollout, which may be more attractive to certain smaller alternative network (AltNet) providers.

Often, Local Supplier Contracts are carved out of the Regional Supplier areas in order to attract more potential suppliers and potentially maximise the pace of delivery in an area. All of these things are complementary, as can be seen by this illustration for Northumberland and Durham:

The first three local supplier procurements under the original Phase 1a areas have already been identified and more will follow.

Mark is a professional technology writer, IT consultant and computer engineer from Dorset (England), he also founded ISPreview in 1999 and enjoys analysing the latest telecoms and broadband developments. Find me on X (Twitter), Mastodon, Facebook, BlueSky, Threads.net and Linkedin.

« Apple TV+ to Launch on Sky Glass and Sky Q Later This Year

i love how they always talk about upgrades in england but i live in scotland and ive been stuck with a 6mbps download and a 0.3 upload for 4 years so ye i can see that the money is going well

Your not alone.

My grandparents live in Lincolnshire they only get around 0.3-0.5MB

Disappointing yet again, not the project itself, but the fact yet again Scotland are lagging.

Has this been stalled due to waiting for the R100 project to finalise plans or is it the failure of Scottish government and councils to get on board.

If English areas are already defining plans and suppliers why aren’t Scottish ones.

Naturally, Scotland will want to see their fair share of funding and to have some say over that. On the flip side, the UK government will be keen to see a more rapid programme than R100. So of course, we have the usual politics and discussions going on behind the scenes. The picture will become clearer soon, I hope.

@Mark

Totally agree, I’d be cautious about allocating funds based on the SGovs performance and decisions regarding delivery under bduk and R100 too.

My pessimistic outlook sees a future where those at the bottom of the adsl chart who saw little or nothing from fttc and again with R100 will also be left out again. We all realise rural is more expensive but it’s easy to just ignore it and talk about the big percentages that did get done.

In SW Scotland gave up on fixed line, 3Mbps down/0.3mbps up, and went 4G, not the best, but much better. R100 saying should get something next year, but not holding my breath; after all originally told better broadband coming soon, which was fttc in village centres in 2014, then told improvements definitely coming in 2017, 2017 “oops we got it wrong”. I have no reason to have any confidence in R100, will only believe it when it happens.

I find it very disappointing that they have effectively abandoned those that still have no superfast broadband. By concentrating on pushing Gigabit, the already superfast areas are being prioritised (for the usual economic reasons) and although some of those may be tackled by this latest plan, there is no sense of urgency – with contracts not expected to start until 2024!

As per the article, “areas with sub-30Mbps speeds will be prioritised, albeit NOT to the exclusion of all else.” They are trying to get to 99%+ coverage with gigabit networks under this programme, while a separate plan is being devised for the final 0.3% of premises where the cost of delivery is simply too expensive.

The sub-superfast properties have been prioritised for the last decade, yet in the Forest of Dean there are still over 13% of properties that are sub-superfast.

The problem with black lines qualifying criteria is they can get silly, I have read today how part of a cul de sac done was done and the rest not.

So 29mpbs means you get FTTP, 31mbps means you stay on FTTC.

So a neighbour getting 31mbps over a neighbour getting 29mbps is not ok, but one getting 1000 and the other getting 31 is?

There is clear flaws in how they are qualifying properties.

Also the terms openreach have to work under, are they allowed to expand a incomplete BDUK coverage commercially? It seems not from what I read, again this be good to clarify, it could effectively means those just outside of a BDUK area are locked out of any commercial rollout for years to come.

Finally we have people in cities with no FTTP, the government seems to think BDUK is only needed in rural areas, and VM is incorrectly been considered as a next gen network when docsis is nowhere near the quality of FTTP.

I guess us rural dwellers should be happy to get any scraps from the table but it doesn’t change the fact that rural properties get their connections years (and in some cases over a decade) after the major centres.

In my fantasy dreamworld it would have been a nice move that they tied city build with a matched percentage of rural development. Want to overbuild in London? Sure no problem but for every 5 or 10 homes you wire up you make you need to make 1 in a properly rural area. You’d soon see the entire country covered and with a far more diverse range of providers. No, I don’t really care that it’s not commercially viable. If we must have a fully capitalist approach they need to be forced to do the non-capitalist things for the benefit of the country. You absolutely can’t rely on them doing it out of the goodness of their hearts not least as capitalism has no heart.

‘In my fantasy dreamworld it would have been a nice move that they tied city build with a matched percentage of rural development. Want to overbuild in London? Sure no problem but for every 5 or 10 homes you wire up you make you need to make 1 in a properly rural area.’

That would just leave no-one covered.

In my fantasy world every major city would have a tube system but here we are.

I don’t suppose there is a more detailed description available of the areas covered? For instance (being selfish) “parts of Cheshire”. I’m also curious how this relates to the Connecting Cheshire website http://www.connectingcheshire.org.uk/category/news/ which shows that Airband was selected to deliver – “Airband will be concentrating on the isolated and rural areas in Cheshire East and Cheshire West and Chester”.

I’d be delighted if anyone taking BDUK money has to open up to other ISPs.

John

I wouldn’t put too much stock in the “open access” requirement, since BDUK aren’t strictly requiring any wholesale solutions to be akin to the products that Openreach offer. In other words, there’s scope for ISPs to game the system by launching a wholesale product, but making it unattractive (we see this already with some networks).

As for more details, those will only follow once we start seeing the first contract awards. However, I really hope that BDUK present this information in a more accessible way to the public, because right now you have to read through long reports just to find the useful details.

Gigaclear are a good example of an ISP making their wholesale products unattractive – their own retail (inc VAT) prices are less than the wholesale (ex VAT) prices, even before other necessary extra costs are added. Yet they satisfy the criteria for making their network available to other ISPs.

Airband now have a detailed checker on their website down to individual premises, so you can see who is in scope and who isn’t.

It was disappointing that the Autumn release didn’t include an update on the current status of the Local Authority Gigabit Voucher top up schemes. I am led to believe that BDUK are finally now accepting new entrants, and that at least one ( Cheshire) had been waiting for this development for the last 6 months.

There seems to be an impression that London has overbuilt Ultra broadband capacity with different companies laying fibre down the same road. Yes FTTC capacity is pretty much ubiquitous here. However, if you takeaway Virgin In outer London then there is hardly any Ultra Broadband penetration. Moreover there are no Openreach or BDUK plans up to December 2026 for this. Take where I live in London Cockfosters/ East Barnet because there is a great big hole in the Virgin network the size of a small town with fibre looking years away. Moreover parts of Outer London could be the last place in the UK to get fibre.

The network builders generally favour housing estate style deployments in towns of the outskirts of cities. Sticking a toby box in the pavement, some ducts under the ground and a cabinet only requires the permission of the local council to dig part of the pavement up, who almost always say yes.

Doing it in London requires talking to TfL, the local borough, etc. Plus dealing with MDUs can really vary, some will let you do whatever, some are fine as long as all cabling is hidden and equipment in maintanence areas, others will refuse for annoying reasons such as only wanting one operator in the building (not including exclusivity agreements).

Still waiting for the results of the Durham / North East OMR to be published… Summer has long since passed.

Basically the number of properties from phase 1 and 2 are being massive slashed, I don’t by the idea that they will all get done via commercial rollouts as Openreach and others don’t always deliver on their promises and some may have to wait 5 years to find out the bad news.