Report Examines Why Openreach’s UK Full Fibre Take-up Beats AltNets

A new report from strategic consultancy firm Eight Advisory has examined the question of why the average consumer take-up across alternative full fibre (FTTP) broadband networks (Altnet) is currently still at 16%, while Openreach stands at c.34%, despite the collective footprint of the new challengers now equalling that of the incumbent.

Network access provider Openreach (BT) recently revealed that their Fibre-to-the-Premises (FTTP) based broadband ISP network had covered 14 million UK premises. By comparison, the Independent Networks Co-operative Association (INCA) and Point Topic recently claimed (here) that Altnet coverage had grown by 57% in 2023 to top 12.9 million premises (up from 49% and 8.22m in 2022).

Despite all this progress, consumer take-up among AltNets is still lagging a long way behind the incumbent on around 16% (ranges from 5 to 30% – based partly on network maturity). At the same time, many Altnets, under pressure from rising build costs, high interest rates and investors, are now increasingly switching their focus from growing build to growing adoption (take-up).

Advertisement

The new paper from Eight Advisory (here), which is actually the first of two new papers (a future second one will propose actionable recommendations to drive penetration), acts as somewhat of a high level summary for all these events and covers a number of the obstacles to adoption, many of which will be familiar to our regular readers.

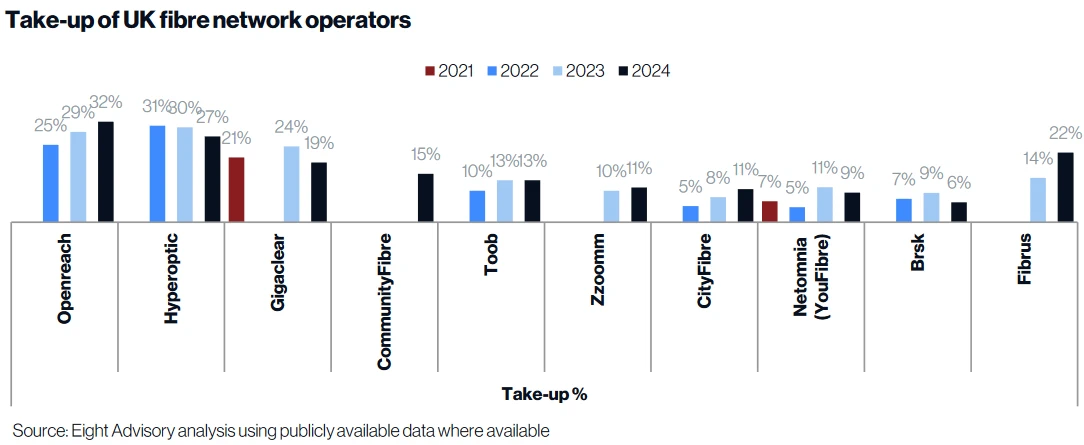

The chart below shows take-up rates of major UK fibre network operators over the 2021 to 2024 period.

Take note that take-up is somewhat of a dynamically scaled measurement, which can be suppressed when a new network roll-out is ramping up and building at a rapid pace. This is why it’s important never to look at a single average % figure in isolation, without context, because the figure may go up or down depending upon the state and age of a build. Take-up also grows organically over time, often taking several years to reach a level of maturity post-build.

Advertisement

Key Identified Challenges

➤ The UK consumer broadband market is highly concentrated on five big ISPs, four of whom buy wholesale broadband from the incumbent Openreach. But Altnets have, apart from CityFibre with TalkTalk and Vodafone, been largely unable to break into this significant route to market. Lack of consumer familiarity with smaller brands is a well-known issue.

ISPr Editor’s Note: In fairness, TalkTalk does in fact sell packages via several other Altnets, such as Freedom Fibre, Community Fibre and a few more. But this isn’t all that well known among consumers.

➤ The proliferation of multiple small networks makes it costly and complex for the larger ISPs to work with Altnets. The much-anticipated consolidation and the integration of networks and IT systems may provide a clearer route for larger ISPs.

➤ Competition at the wholesale level is expected to grow once Virgin Media opens up their national broadband network in the near future (here), which could make it even harder for Altnets, especially if some of the bigger ISPs choose VMO2 over smaller alternatives.

➤ The longer established Altnets report average take-up across their networks of around 30% with fluctuations impacted by changes in rollout speed and some churn. Hyperoptic and Gigaclear show that convincing people to move to a full fibre service takes a long time and consistent marketing effort. Neither currently sell through wholesale.

As with the longer established Altnets, in established footprint take-up can be much higher. In Stirling, CityFibre state their penetration has exceeded 23% and in Milton Keynes, its most mature network footprint, penetration has now passed 27%. As with any average, some areas will be lower.

ISPr Editor’s Note: Technically Gigaclear does in fact do a wholesale product, although only a few ISPs (e.g. Squirrel Internet) seem to sell this. But that’s not surprising given the vertical integration of Gigaclear and their lack of incentive toward offering a truly fair, accessible and competitive wholesale propostion (i.e. like Openreach or CityFibre).

As we say, the paper doesn’t go into a lot of detail or contain any surprises, but it does provide for a simple overview of the current state of affairs.

Partner of Eight Advisory, Nick Breadner, said:

“Driving penetration & takeup is one of the number one goals of UK altnets. The expected consolidation will shake up both the retail and wholesale markets but the combined challenges of agreeing valuations, manging integration at the network, operational and commercial levels, and onboarding new larger ISPs will provide new challenges for altnets and the emerging consolidators”.

We look forward to seeing the next paper, which is arguably going to be much more interesting, particularly given its promise of recommendations. On the other hand, we would have much rather seen a single paper instead of splitting it up in this way. Otherwise, it will be interesting to see how much of what they may recommend ends up echoing the previous GigaTAG report from four years ago, which looked at the same issue.

Mark is a professional technology writer, IT consultant and computer engineer from Dorset (England), he also founded ISPreview in 1999 and enjoys analysing the latest telecoms and broadband developments. Find me on X (Twitter), Mastodon, Facebook, BlueSky, Threads.net and Linkedin.

« Shortlist of Network Operators Named for the UK Fibre Awards 2024

Oops sorry about the Gigaclear gremlin – entirely my fault. On TalkTalk, I should have been clearer about “largely unable” as I can see how it has been interpreted.

I’m glad you enjoyed it and are looking forward to our follow up paper.

Chris (Co-Author)

The fact that it’s actually available helps a great deal…

I sort of agree. The uptake percentage is more an indication of demand/sales than of availability.

The probable reasons for the report are:

1. Their figures are double those of competitors.

2. They are building at a very high rate; maintaining such an uptake rate is a massive achievement when the pace of construction is so rapid.

The reasons I would say this is the case:

1. Openreach is deploying to areas where only they can make a profit and where current provisions are poor. Consequently, when the service becomes available, people adopt it very quickly.

2. Most of the funding for hard-to-reach areas has gone to Openreach.

3. Even when there is a choice between an alternative network (AltNet) and BT, customers are opting for BT suppliers over AltNets.

4. BT supplies at the wholesale level more than any AltNet does.

Facing facts, BT still holds a monopoly over fixed telecoms. CityFibre had the best chance of challenging them, but now that BT has aggressively pushed FTTP, it seems unlikely that an AltNet will succeed. The beast is too big and mighty.

I sort of agree. The uptake percentage is more an indication of demand/sales than of availability.

The probable reasons for the report are:

1. Their figures are double those of competitors.

2. They are building at a very high rate; maintaining such an uptake rate is a massive achievement when the pace of construction is so rapid.

The reasons I would say this is the case:

1. Openreach is deploying to areas where only they can make a profit and where current provisions are poor. Consequently, when the service becomes available, people adopt it very quickly.

2. Most of the funding for hard-to-reach areas has gone to Openreach.

3. Even when there is a choice between an alternative network (AltNet) and BT, customers are opting for BT suppliers over AltNets.

4. BT supplies at the wholesale level more than any AltNet does.

Facing facts, BT still holds a monopoly over fixed telecoms. CityFibre had the best chance of challenging them, but now that BT has aggressively pushed FTTP, it seems unlikely that an AltNet will succeed. The beast is too big and mighty.

I suppose most people all started off on FTTC (Openreach) with an ISP selling openreach fttc products. Or they are on Virgin Media. So they may only know they can upgrade to fttp when their current isp tells them. Perhaps they are on fttc, then one day an altnet starts to build in their street. They may have just renewed their fttc contract with their isp for another 2 years. So they may wish to switch to the altnet, but then they’d have to pay early contract cancellation penalties. If it was openreach building in their street, their current isp may allow them to upgrade from fttc to fttp without penalty. Another factor I think is that the comparison sites loke Uswitch only tend to show Openreach and Virgin deals at one’s address. So even if an Altnet’s service was ready to order in your street, you wouldn’t necessarily know this by just going onto a price comparison site. You would only know if the Altnet dropped leaflets through your letterbox or you saw their name and them working in your street. Or you are tech savy and consulted roadworks maps or say Better Internet Dashboard.

One of the big challenges for AltNets are consumer contracts, especially if Openreach FTTP arrives at a similar time. Consumers won’t jump to an AltNet if they can’t get out an existing broadband contract but they might upgrade to FTTP via their existing ISP without penalty. Openreach ISPs are incentivised to do this through the Equinox contract. I bet OFCOM missed this when they approved the Equinox proposal

some altnets offer to buy out your remaining contract, which is a bit odd as they’ve giving money to rivals for providing no service

They’re not giving *anything* to rivals.

They’re giving a free ride to *their own* customer for a certain number of months, sure – but they are also gaining a customer who will be paying for the remainder of the contract period, and quite possibly long afterwards (once you’ve got the ONT installed into the property, it’s much easier to retain the customer)

Also, their network which passes the property is otherwise sitting idle, so they may as well be using it. The incremental cost of serving a customer is very small, but the cost of building the network is very large.

Choice of a network that is supported by multiple ISPs with keen competitive prices with the ability to swap between them as contracts end. Verses. Small altnet that may or may not be here tomorrow, offering a low price, and the need to drill another hole in the wall and have a different ONT.

For many people I guess the choice is simple

The Gremlins have now been sent to bed and the report updated accordingly on our website – thanks Chris

Thank you for writing this!

I assume it is a simple conclusion – ie, Openreach had lots of existing customers and moving them to FTTP within their existing contract framework and supplier was far simpler than getting people to switch to a new supplier and exiting an existing contract

I’m not even sure they’re marketing correctly. Hey Broadband/F&W Networks launched in our street only a few months ago and is the only FTTP in the area but I have seen no marketing at all, maybe it’s still too new? – I only knew it was coming because I work from home and saw their vans wiring the street last year!

Personally very happy so far and they gave “free” service for the time our VDSL/FTTC contract has to run.

A village close by me has had an altnet in place for months. No customers though as no one knew about it aside from road works (just an annoyance in small places) and a singular leaflet drop.

Virgin is now building and in comparison have made themselves very well known locally.

@MarkJ

I’m pretty sure that the TBB analysis of the INCA coverage numbers showed it included a fair amount of duplication through overbuild and that the number of unique premises was somewhat lower. This will impair combined altnet take up calculations as they are competing with themselves in some cases.

It in my view comes down to the government using the wrong approach, Most people were with the incumbent operator which of course is BT so they are likely to remain with them. Another problem with Alt Nets is not all offer a landline and those that do you may not be able to retain your existing number

A further issue is you gave less choice you are locked into that one altnet and switching is difficult where as with BT multiple ISP’s will provide the service and switching is a bit easier

If as I expect most of the altnets consolidate that may change the situation. It is pretty clear to me that the current low take up of the altnet services means they are not in the long term finabciallyu viable

Do you have to change routers if switching ISP but staying on Openreach?

Clive, you don’t need to change the ONT on the wall, but the ISP will send out their own router. The changeover is therefore as simple as unplug one, plug in the other, with no drilling or other disruption

1 Brand awareness,

2 Wariness of Altnets going bust

3 Risk of being locked into a contract with an unreliable ISP / oddly implemented ISP

1. Everyone knows who BT is, they’re a FTSE 100 company. They also used to be publicly owned, so there’s residual “they’re the default” attitude.

2. Are you sure that if you sign-up with “WoOooOoo Badger!” (a company that nobody had heard of 2 years ago) that they will still be in business in 2 years time?

3. Are you sure that they don’t use some weird thing like CGNAT, or that they have provisioned enough backhaul?

People are very demanding about the reliability of their IP supply. Much as we like to complain about BT/OR, that’s because we hold them to a higher standard. (See also pace of FTTP rollout). You can (except for unusual circumstances) rely on OR to provide you with a reliable service.

Brand awareness works both ways against BT. Many know it is poop. I for one will change as soon as I can

Arg, what happened to my line breaks?!

For context, the site renders your post differently when it’s in the moderation queue to how it’s rendered when authorised.

The recent activity by an alt-net has its own isp, no other choice afaik. The contender alt-net has not appeared at all. OR, no activity either.

Based on the number around here on substandard fttc broadband, first past the post will probably do well.

The first alt-net has rodded / roped most of the area, and a small green cabinet is present, with a larger, ffc sized cabinet planned.

Anybody know what would be in the various cabinets, located at the same location?

Another factor is Fibre Priority exchanges (copper stop sell); customers in those areas will be strongly encouraged to migrate to FTTP on next contract renewal, and that will increase Openreach FTTP take-up for users who want to stick with their existing ISP.

There is of course a large majority of people who don’t *care* about FTTP; >95% of the country has FTTC available and for a big chunk of those it’s good enough. They will only migrate to FTTP if it’s cheaper than what they currently pay, or they have no other option.

When I lived in Newcastle, I was on Wideopen exchange and despite that Openreach When and Where saying it’s not a fibre build exchange yet, most of the Gosforth addresses on that exchange are FTTP

When my Sky Broadband contract came to an end they offered it at the same price as FTTC and they had an offer that if you took Netflix with Sky, they would discount the FTTP by a further £8 cancelling out the Netflix charge, so you got Netflix free. Upon renewal 18 months later, they offered the exact same deal at the exact same price however, I moved 4 months later.

I am now on FTTC just outside of Alnwick but Sky retained the offer on my account and said when we go FTTP later this year, I can have the FTTP back and retain the Netflix. This makes it a lot cheaper than the alnet here which is Go Fibre who have just installed their FTTP last week in the village and due to go live in the summer. Go Fibre are £39 too for the 500mb service compared to Sky at £34 and if I drop Sky FTTC/P, I will have to pay for Netflix too so that’s a big difference over a year. This is one advantage that the altnets don’t have

@jazzy GoFibre will also saddle you with CGNAT for more than an Openreach ISP will charge. One thing they do offer is upgrade to symmetric for £5 a month which is a good deal

1 Door to Door sales.

2 Reluctance to have garden dug up.

3 Lack of demand for faster speeds.

4 Sky are on Openreach.

Would like to see Virgin data as they appear to be expanding network but customer numbers are static. Altnet effect on Virgin does not seem to have been looked at much.

Perception of reliability may play a part. BT and Openreach border on disfunctional at times, but they will ultimately fix a fault. People are seeing delayed, haphazard and low quality rollouts and concluding it’s better the devil they know. My personal opinion – the Altnets also do a great job of avoiding areas where they could maximise uptake.

This isn’t that surprising…

Lots of folk will NEVER switch from BT (especially over 50s). I’m sure we all know examples, I can think of 10 people I know that, well… they just couldn’t. Given any choice, they’ll stick with BT.

Then the idea of not using a “normal” landline, ever though they rarely use it, heads will start to spin. Altnets… forget it.

My neighbour recently complained about his BT bill being £120 a month. This is just phone and broadband on VDSL, no TV package.

I was flabergasted, many times I’ve spoken about alternatives. I sent him a link to a sub £25/m deal.

A few days later he said he called BT, he was happy, they’d given him a big discount, still over £70. His words, “you can rely on BT”.

Two weeks later I switched to a £17/m deal.

Which makes it all the more strange that BT have *chosen* to scrap their branding for retail. Insane

I’d love to switch to the AltNet (Grain) that’s available at my home, but unfortunately, due to their business decisions of locking down their equipment, and not allowing any access to it, I won’t be going near it. You actually have to phone them up to get them to adjust the settings to let you plug your own router into their hardware. Fortunately, I have Openreach FTTP available too, so I use an ISP via that, where I can control the hardware (with exception of the ONT).

Yes, it’s surprising that the smaller providers I’m the UK aren’t more flexible for tech users.

Yes, very strange that. Some altnets policies would make me think again.

It’s bonkers that you can’t run all internet “services” in your own home.

Blocked ports etc… it’s not really “the internet”, but some watered down web browsing service.

Not overly surprising given how crap the systems are, I’ve had Vodafone via CityFibre since it went live in my area about 2.5 years ago. The Cityfibre site says talktalk is an available isp, if I go via them or direct to talktalk the most it will offer me is Fibre 65. If the ISPS that are supposed to do it aren’t even offering it then how will people know to switch.

As I’ve said before on this site perhaps if the altnets developer a common wholesale platform and presented themselves as a unified access product to co pete with Openreach they would do themselves one hell of a favour.

One network selling wholesale with multiple ISPs aggressively marketing services, versus multiple networks mostly with just a single service to market with partial coverage, big differences in service offering and lack of established name.

Not exactly rocket science to figure out why the uptake is lower.

Customers on OR infrastructure already will be encouraged to move to FTTP products as wholesale cost to ISP on FTTC is greater than FTTP product, hence the marketing from BT and Sky that they will upgrade you for “free” when FTTP becomes available as their margins will increase just by moving customers from FTTC to FTTP.

Just finished at a customers where I’ve been adding to their garden deck. This morning they have a person around trying to sell them an ‘AltNet’ FTTP package – they sent the AltNet person away with a ‘flea in their ear’ as the whole road is between ‘fed-up’ to furious at the hassle, muck and disruption from the amount of work that has gone on in the last 18 months from not 1 but 2 AltNet’s digging up the verges, road and blocking peoples driveways with the construction work to fibre up the road. They already have BT/OR FTTP and Virgin in the road, provided in the existing ducts.