KCOM’s UK Results Reveal Huge £530m Write Down in Value of its Assets

The incumbent broadband and telecoms provider for Hull, KCOM, which has also built their full fibre (FTTP) network across other parts of East Yorkshire and Lincolnshire (England), have published their annual accounts to 31st March 2025 and revealed a huge c. £530m write down in the value of their assets. The results give context to the company’s new capital restructuring deal.

Just to recap. Macquarie Infrastructure (MIRA / MEIF 6 Fibre) secured their £627m acquisition of KCOM in August 2019 (here) and promptly began a major network expansion, while also selling off some of the company’s assets. But since then the operator’s dominance of their core market in Hull, were Ofcom still deems them to hold Significant Market Power (SMP), has been eroded by rival networks.

According to Ofcom, recent fibre builds by rivals like MS3, Connexin (now part of CityFibre) and Grain have given local customers more choice of broadband connectivity, with around 70-79% of premises in the Hull Area now having access to at least one alternative network to KCOM. In addition, the regulator’s proposed plan to maintain many of its controls on the incumbent and even foster greater infrastructure sharing won’t have helped (here).

Advertisement

Regular readers might recall that Macquarie also kicked off a Strategic Review of the business back in the Spring of 2024 (here). The development was then followed in February 2026 by reports that Macquarie had allegedly taken another step toward consolidation by appointing Perella Weinberg Partners to test the UK market for interest in a sale of KCOM’s business (here), possibly during Q2 2026.

All of this helped to explain ISPreview’s report at the end of March 2026, which revealed that KCOM had struck an agreement with their lenders and shareholders to restructure their current capital structure (here). In short, KCOM was struggling with its debts (not uncommon in this market) and attempted to resolve that, for now, by capitalising interest (i.e. shifting interest charges to debt/loans for payment later) and resetting covenants (i.e. lenders have probably relaxed the rules to be more flexible). Essentially, a temporary fix until September 2027, rather than a permeant one.

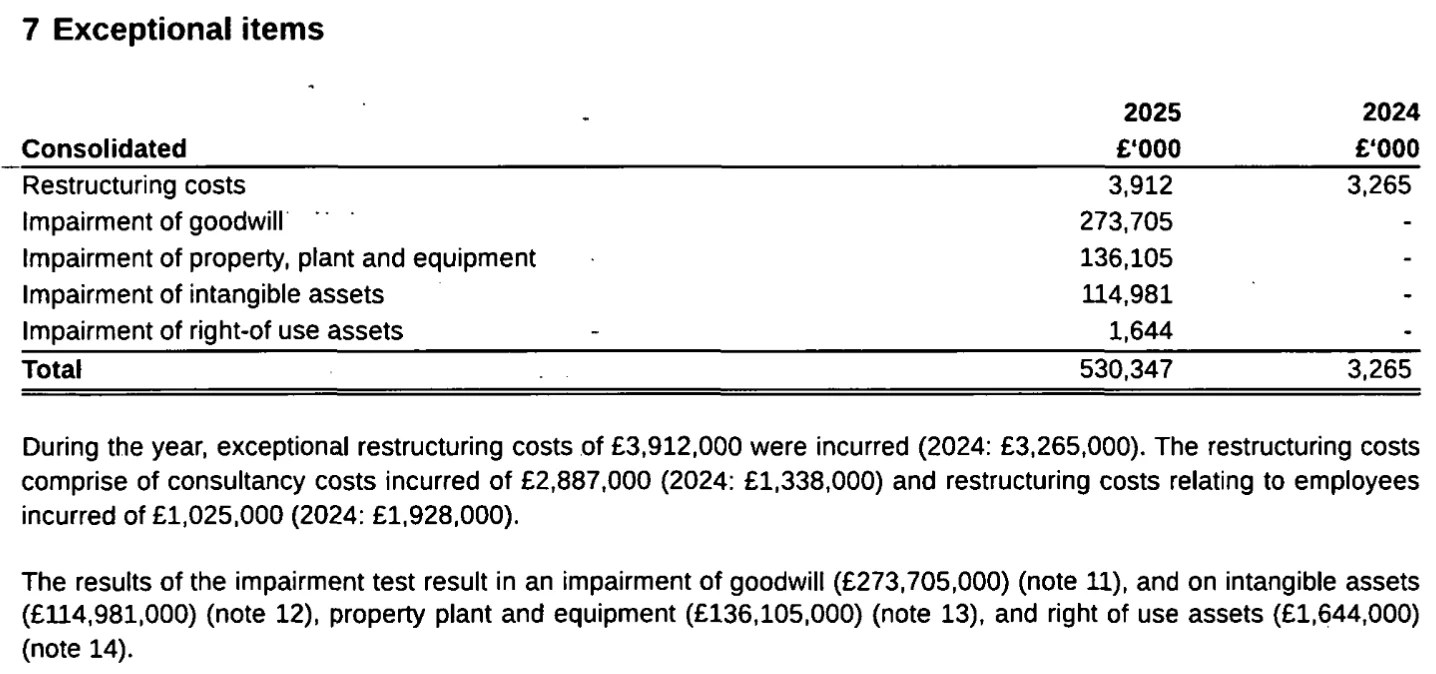

However, last month’s news lacked the detailed financial context for the aforementioned agreement, which KCOM Group Limited has now revealed by publishing their annual results for the year to 31st March 2025. Sadly this doesn’t provide any solid information on how many broadband customers they still have or their latest FTTP network coverage figures, but the financial data is quite revealing. We’ve summarised this below.

Summary of KCOM’s Key Results to 31st March 2025

➤ Revenue fell 5.6% to £96.2m

➤ EBITDA fell 5.9% to £39.9m due to “cost saving initiatives”

➤ Operating expenses reduced to -£77.74m (2024: -£91.77m)

➤ Operating profit before exceptional items increased by £8.185m to £18.62m, albeit mostly due to the sale of surplus assets. But those exceptional items hit -£40.33m (2024: -£3.26m).

➤ Loss before tax skyrocketed to -£31.22m (2024: -£1.62m), giving a total loss for the year of -£25m (2024: -£163,000)

➤ Total assets for KCOM were worth £210.72m (2024: £236.19m)

➤ Total liabilities hit -£205.64m (2024: -£204m)

➤ There was a loss of -£468.73m for the parent company in the year (2024: £nil)

➤ KCOM’s total employee count fell to 697 (2024: 765)

However, the ultimate UK parent company is KCOM Holdco 1 Limited, which ISPreview notes reported a staggering operating loss of -£535m for the year (2024: -£17.91m). The list of “Exceptional items” is also particularly revealing and shows that the parent company has taken a huge c. £530m write down in the value of their assets (total recorded accounting impairment, albeit somewhat inflated by holdco layering effects). The report also noted a loss before tax of -£596.5m (2024: -£67m).

Advertisement

The above helps to show why Macquarie are now busy testing the UK market for interest in a possible sale of KCOM’s business (the best outcome) and, ideally, they’d want to find a proper solution this year, well before September 2027. Some alternative options might involve debt restructuring (i.e. lenders taking more control of the company) or a break-up / asset sale of the business. We’ve approached KCOM for a comment this morning and await their response.

Mark is a professional technology writer, IT consultant and computer engineer from Dorset (England), he also founded ISPreview in 1999 and enjoys analysing the latest telecoms and broadband developments. Find me on X (Twitter), Mastodon, Facebook, BlueSky, Threads.net and Linkedin.

Advertisement

Leave a Reply

Privacy Notice: Please note that news comments are anonymous, which means that we do NOT require you to enter any real personal details to post a message and display names can be almost anything you like (provided they do not contain offensive language or impersonate a real person's legal name). By clicking to submit a post you agree to storing your entries for comment content, display name, IP and email in our database, for as long as the post remains live.

Only the submitted name and comment will be displayed in public, while the rest will be kept private (we will never share this outside of ISPreview, regardless of whether the data is real or fake). This comment system uses submitted IP, email and website address data to spot abuse and spammers. All data is transferred via an encrypted (https secure) session.

What a shame. My heart weeps for Macquarie…..not.

If anyone still wonders why KCOM didn’t want to allow PIA on their network here you are.

Wouldn’t be surprised if having no infrastructure competition was responsible for half the value of the entire company.

It has to go down as a fail by Ofcom that they didn’t impose the same PIA terms on Kcom that they did on Openreach.

Not sure I agree with that Big Dave. Look at how the OR PIA costs have changed over time. The initial PIA pricing with a much smaller customer base to spread the fixed costs of building a PIA model would surely have been unworkable.

More fibre for sale in this country than a warehouse of All Bran.

Why not sell to BT Group and have the network arm transferred to Openreach?

I would imagine that there is no great incentive for BT Group to take it on. It’s always been an anomaly, it can remain one

This company had a monopoly and they are still losing money

They had a monopoly with Thames Water too.

Look how well that went … not!

This group of companies must be run by a bunch of complete proverbials.

If you read the story properly. When they bought the company, there was next to competition. Now roughly 80% of the properties they were the only provider to, now have options via MS3 and or Cityfibre.

That’s why they’re now losing money