Study Highlights UK Competition Challenges of Netomnia’s Acquisition by Nexfibre

A new study from Point Topic has examined the impact on infrastructure level competition from nexfibre’s £2bn move to acquire full fibre broadband operator Netomnia (here). The analyst suggests that consumers in overlapping areas could see reduced infrastructure-level competition and less aggressive pricing over time, which may impact the Competition and Markets Authority‘s (CMA) assessment of the deal.

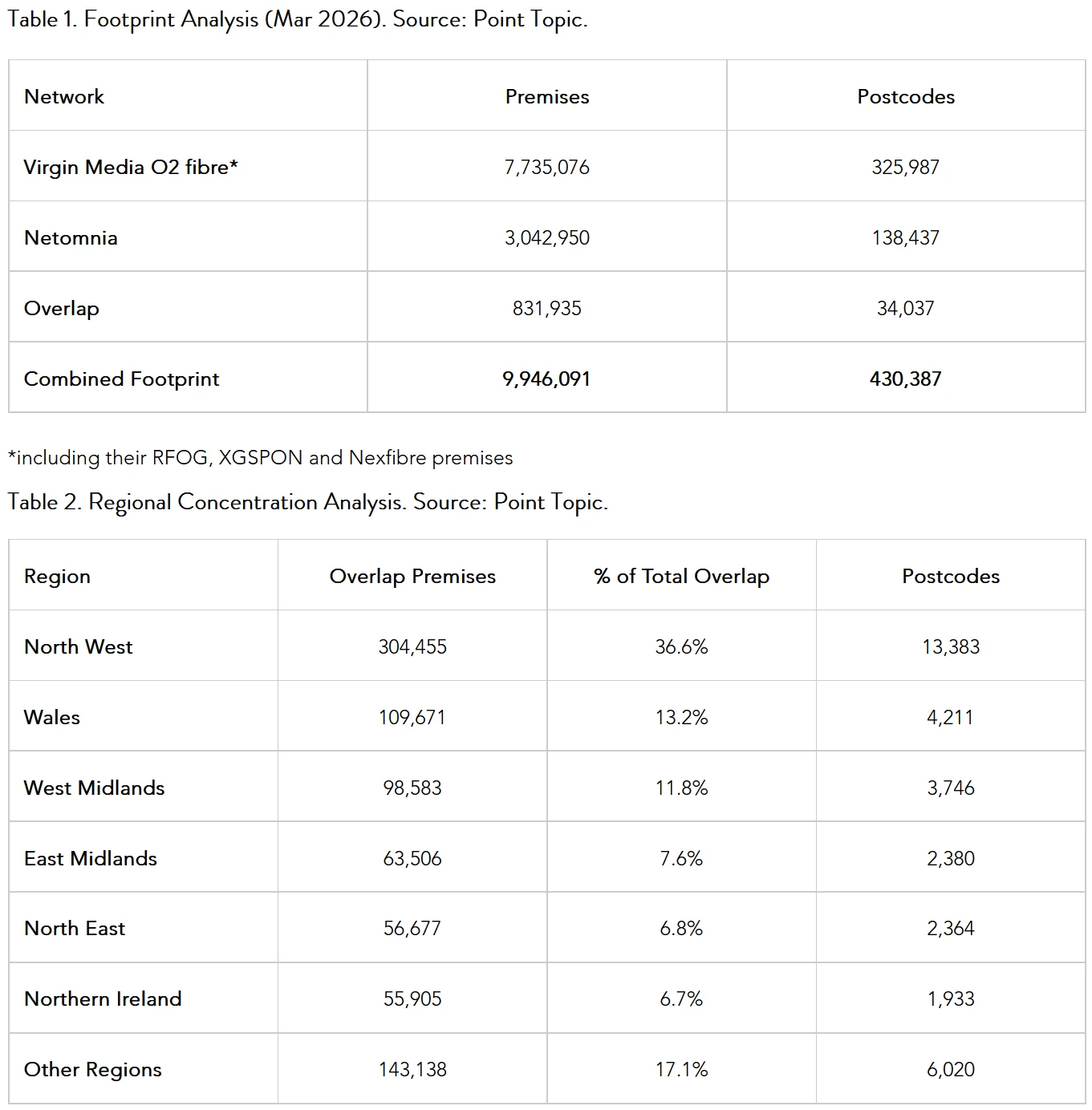

Just to recap. The owners of nexfibre (InfraVia, Liberty Global and Telefónica), which shares some of its parentage with Virgin Media and O2, announced in February 2026 that they’d reached a £2bn deal to acquire Netomnia (here), which had at the time already deployed their own full fibre network across 3 million UK premises (rising to c.3.4m premises and 500k customers by deal completion – expected by Q3 2026).

Nexfibre said the deal would unlock £3.5bn of investment in the UK market and help to upgrade 2.1 million of Virgin Media’s premises from coax (HFC) to full fibre (FTTP). The combined nexfibre and Netomnia footprint is expected to reach 8m premises by the end of 2027, which when combined with Virgin Media’s network could collectively reach 20m premises (c.10m if only looking at FTTP) and create a “scaled, financially secure challenger to BT Openreach“.

Advertisement

The deal has been promoted as one that could improve competition for national incumbent Openreach. But telecoms analyst firm Point Topic finds that in areas of existing overlap (overbuild) between the networks – equating to around 832,000 premises and 34,037 postcodes between Virgin Media O2/nexfibre and Netomnia – the story could be quite different.

According to the report, consumers in overlapping areas could see “reduced infrastructure-level competition, less aggressive pricing or promotional activity over time, lower pressure for network upgrades and service innovation, and reduced long-term competitive tension between independent fibre builders“.

On the other hand, the national impact of this may be limited. The overlap analysis indicates that fibre competition is highly concentrated geographically (particularly around the North West, Wales and parts of the Midlands), rather than evenly distributed nationally.

Advertisement

The North West alone accounts for approximately 40% of all high-competition overlap premises, with Wales representing the second-largest concentration. Major urban authorities, including Liverpool, Manchester, Birmingham and Belfast, contain particularly dense clusters of competing FTTP infrastructure.

In addition, of the 34,037 overbuilt postcodes, some 91.6% (766,554 premises) are classified as “high-competition” areas with 5+ fibre operators. “At first glance, this might suggest that consumers in these areas benefit from substantial infrastructure competition,” but Point Topic points out that, in practice, much of the underlying infrastructure competition in these areas may reduce to Openreach-based networks and Virgin Media/nexfibre/Netomnia infrastructure.

Point Topic Statement:

“The analysis highlights an important distinction between retail broadband choice and underlying network competition. Although many overlap areas appear highly competitive based on the number of consumer-facing broadband brands available, much of that retail competition is supported by the same underlying Openreach infrastructure.

At the same time, the data also reflects the broader structural challenges facing the UK fibre market. Many of the overlap areas are already highly saturated, with extensive infrastructure overbuild and limited remaining headroom for subscriber growth. Against that backdrop, the parties are likely to argue that consolidation may improve long-term network sustainability and strengthen competition against Openreach at a national scale.

Ultimately, the CMA’s assessment is likely to turn on whether fibre competition is viewed primarily through a national retail market lens or through a more granular local infrastructure framework. The regulator’s approach in this case may not only determine the outcome and timetable for the nexfibre/Substantial transaction, but also set an important precedent for how future Altnet consolidation is assessed across the UK broadband sector.”

At present the CMA are only in the evidence gathering stage, although it would not be surprising if they then proceeded to an initial Phase 1 review process. The real question is whether or not they then conclude that there is a need for a deeper Phase 2 investigation, which could push deal completion into 2027 and might potentially require VMO2/nexfibre to make some concessions.

Passing Phase 1 usually requires the CMA to conclude that there is no “realistic prospect” of a significant lessening of competition from the deal, which is a tougher standard to meet than the Phase 2 “balance of probabilities” test. However, given the CMA’s recent flexibility toward big telecoms mergers (e.g. Three UK and Vodafone) and the Government’s broadly favourable response to the deal, it’s not unreasonable to expect that they may ultimately allow the consolidation to go through.

Advertisement

Quite what form any concessions, if they do indeed materialise, may take is as yet unclear. But as we’ve said before, we would not be surprised if it included stronger wholesale requirements for Virgin Media’s consumer broadband network and nexfibre, which is something that those operators already seem to be preparing to try and deliver (here and here). Time will tell and at present there’s still a fair bit of uncertainty over the final outcome.

Mark is a professional technology writer, IT consultant and computer engineer from Dorset (England), he also founded ISPreview in 1999 and enjoys analysing the latest telecoms and broadband developments. Find me on X (Twitter), Mastodon, Facebook, BlueSky, Threads.net and Linkedin.

« UK ISP TalkTalk Business Set to Relocate to a New Salford Headquarters

Advertisement

Leave a Reply

Privacy Notice: Please note that news comments are anonymous, which means that we do NOT require you to enter any real personal details to post a message and display names can be almost anything you like (provided they do not contain offensive language or impersonate a real person's legal name). By clicking to submit a post you agree to storing your entries for comment content, display name, IP and email in our database, for as long as the post remains live.

Only the submitted name and comment will be displayed in public, while the rest will be kept private (we will never share this outside of ISPreview, regardless of whether the data is real or fake). This comment system uses submitted IP, email and website address data to spot abuse and spammers. All data is transferred via an encrypted (https secure) session.

Maybe they could require VMO2/Nexfibre to sell on the bits of Netomnia which overlap with existing VMO2/Nexfibre fibre build, although whether a third party (eg CityFibre) would be able to practically integrate such assets into their own network would be doubtful. Rajiv Datta has already said he thinks there’s only room for 2 national players.

All noise, to make it look like a report has been considered.

VM seem confident this will pass having threatened to stop building out fibre, they’d only say that if they were confident they wouldn’t have to…

No this is just an illusion, the deal will still get rubber stamped for approval, hence why window of feedback was so small. After the 3/Voda merge and what is starting to happen already there with speed caps so soon, this is just window dressing….

Point Topic aren’t the CMA. How does your comment make any sense in relation to this Point Topic report?

this reports viewpoint really depends on who paid for it, such at BT and Openreach. just to raise issues which dont exist.

This argument “oh in overlapping areas there may be less competition” is silly because it then raises the point that the entire UK should be overlapped

The argument that it discourages upgrades also does not make sense as XGSPON is THE upgrade

The sector needs to consolidate to survive in the long term. I know most of use despise Virgin Media but that isn’t a reason to block the deal. There are going to be many mergers of this kind over the coming years. The important thing is that at the end of it there remains a couple of serious competitors to Openreach.

VM’s only point for take-over is to STUB OUT the competition and prevent CityFibre having it, which for most is a better consolidator to take-over Netomnia.

If you’ve been a previous customer of VM, you’ll be well aware why so many avoid their dubious operating practices….and they can’t even deploy IPv6 at a technical level…..

Ah here we go again.

VMO2 aren’t buying Netomnia, nexfibre are.

nexfibre don’t provide IP so IPv6 not relevant there.

Netomnia don’t either, YouFibre do.

The idea VMO2 couldn’t enable IPv6 if they chose to is laughable. Even if somehow there were no-one capable in the UK both of their parents have deployed it and worst case they could pay contractors. It’s a purely commercial decision not a technical one.

I have Youfibre, VM runs across the road and literally leaves the pavement outside my gate. So I can’t get it but my next door neighbour can get both. They didn’t want to do the estate to the back of me so they skipped it.

I very much doubt they will correct that – so the whole thing is stupid

There’s a few million other premises besides yours involved but either way there’s no need to change anything in the local area to allow VMO2 over what was the Netomnia network and YouFibre over VMO2 FTTP.

Polish Poler – Not sure how or why you advocate a defence for not implementing IPv6. Its long overdue and has been around for a few decades now. And I don’t believe it’s completely a commercial decision, after VM had looked at it via DS-Lite a half baked non-native IPv6 and gave up. How is it other ISP’s manage to enable IPv6?

Pedantic over who is buying too. Nexfibre might be buying but WHO is a major owner of Nexfibre – its VM or VMO2 whatever name you want to call it!

Also pedantic over Netomnia and YouFibre as at this moment in time they are the same thing, just operated under separate names, but both owned by Substantial Group.

‘Not sure how or why you advocate a defence for not implementing IPv6.’

Just as well I didn’t so you’re all good.

‘And I don’t believe it’s completely a commercial decision, after VM had looked at it via DS-Lite a half baked non-native IPv6 and gave up.’

Whether you believe it or not is irrelevant.

They moved to planning dual-stack instead, for technical and commercial reasons. Waiting on the bean counters to open the purse strings as people only have so much time and for now they’ve ample IPv4 space.

Thinking the second largest network in the UK couldn’t implement IPv6 remains laughable. Even if they couldn’t they could pay a third party services organisation or even their vendors’ professional services to do it. They aren’t due to… ‘commercial decisions’.

As an aside bringing up VM looking at DS-Lite, a ‘half baked non-native IPv6,’ isn’t helpful to your credibility on VMO2’s technical ability to deploy IPv6. DS-Lite is native IPv6, the non-native part is the IPv4: it rides over IPv6.

‘Nexfibre might be buying but WHO is a major owner of Nexfibre – its VM or VMO2 whatever name you want to call it!’

Nope. VMO2 don’t own any part of nexfibre.

‘Also pedantic over Netomnia and YouFibre as at this moment in time they are the same thing’

News to Netomnia and YouFibre. They’re different companies with different staff and separate responsibilities owned by the same parent. The group was literally built to ensure they were not the same thing.

So in streets where YF is there- but VM is not but in the next one over. Will this deal allow VM to be desployed there too? Or can a YF customer go to say giffgaff ?

if not why not?

Eventually… Doubt it will happen overnight on the day the takeover happens. But eventually netomnia will become nexfibre, and then you will be able to order any ISP avalable on the nexfibre network.

Yes, pretty soon.

I have objected to the CMA.

If we allow VMO2 or Openreach scoop up any competition, then we will end up with a infrastructure Duopoly, which is not healthy for competition. I am itching to get away from Virgin when m contract ends now BRSK are in my area.

Plus I do not want to keep having to accept these contract rises all the time. I believe if you agree to an 18 Month contract at a certain price, it should stay that price during the full length of your contract.

brsk is now all youfibre.

and you’d be jumping onto the same network that vm02 will be using too.

When will the UK get it, they have already milked all the money out, C level please stand up, do you all understand that fibre networks need maintenance, especially those sitting in water. The 5% to 30% you have customers on paying below EBITDA needs to be looked after , but so does the rest of it, non used networks deteriorate at such a fast level investors will need to double financial input, extend loans and forget ROI. Give it to Irish to run, they do well out of FTTH.

I guess City Fibre wouldn’t have made the Netomnia shareholders as rich.

That’s all it ever boils down to.

The only people who had their shares triggered were about 10 people half of which from Brsk to allow the merger to happen and keep their jobs!

The only individuals who had their shares triggered were about 10 people half of which from Brsk to allow the merger to happen and keep their jobs!

If you were selling your house, would you accept the best offer or the one that was most popular on an internet forum.

They took a deal that paid only certain people nothing to do with the amount

I would be surprised if the CMA totally blocked the purchase. If they do approve the purchase, I hope they will put the condition of a wholesale access model across VMo2’s entire FTTP footprint a la OpenReach. I am sure I can not be the only person that would like to have the choice of and additional FTTP network (other than OpenReach) with a choice of providers, if for nothing else than redundancy and of course not having to use VMo2 themselves. Especially if symmetrical speeds do not require an OTT payment as currently VMo2 are the only provider in my area with a symmetrical option on FTTP and I REALLY do not want to get back into bed with the devil himself.