BT Group Grows FTTP Broadband Coverage to 5.2m UK Premises

The BT Group has today reported their latest Q1 2021/22 results, which among other things reports that Openreach’s 1Gbps capable Fibre-to-the-Premises (FTTP) broadband ISP network now covers 5.16 million UK premises (up from 4.6m last quarter) and 860,000 of BT’s retail ISP customers have taken the service.

As usual, it’s been another busy quarter for the operator. Over the past few months BT has begun to replace Huawei’s 4G and 5G mobile kit (here), they’ve trialled a new hollow core fibre optic cable (here), launched the next generation of their Street Hub kiosks (here), introduced a new Pay TV set-top-box (here), reintroduced optional 12-month contract terms (here) and seen Altice UK gobble a 12.1% equity stake in the business (here).

On top of that, BT has signed a deal with OneWeb to potentially harness their LEO satellites for rural broadband (here) and they’ve also launched a new low-cost social tariff for those on benefits (here). Meanwhile, Openreach have published the first reference offer for their new Dark Fibre Access (DFA) product (here), while also suing Tii Technologies over faulty ADSL kit (here) and tweaking stop sell rules in copper to fibre migration areas (here).

Advertisement

Elsewhere, Openreach has appointed CommScope to supply some of its FTTP kit (here) and continued to expand their FTTP rollout programme (here), while also launching a major new discount for UK ISPs that take the same broadband service (here). On top of that they’ve also become one of the first UK operators to trial Nokia’s new 25Gbps PON kit (here).

Finally, Ofcom also ordered BT to improve their 10Mbps Universal Service Obligation (USO) for broadband (here) and the operator also managed to avoid the risk of a major national strike by the CWU (here), at least for now.

Financial Highlights – BT’s Quarterly Change

* BT Group revenue = £5,070m (down from £5,286m)

* BT Group profit after tax = £2m (down from £196m)

* BT Group total net debt = £18.566m (increased from £17,802m)

BT doesn’t report full customer figures for their own retail broadband ISP division, but they have started doing it for their ultrafast services. BT Consumer reported that they had 860,000 FTTP customers (up from 753K last quarter) and EE’s “5G Ready” base now stands at 4.088 million (up from 3.261m).

Meanwhile, some 82% of BT’s fixed consumer base now take a “superfast broadband” service (down slightly from 82.4% last quarter as customers move to FTTP) and this drops to just 6.6% (up from 5.5%) for their “ultrafast broadband” (100Mbps+) products (this covers both G.fast and FTTP technologies).

Advertisement

We also noted that some 21.5% of BT’s consumer and business customers are now on converged products (i.e. mobile and broadband).

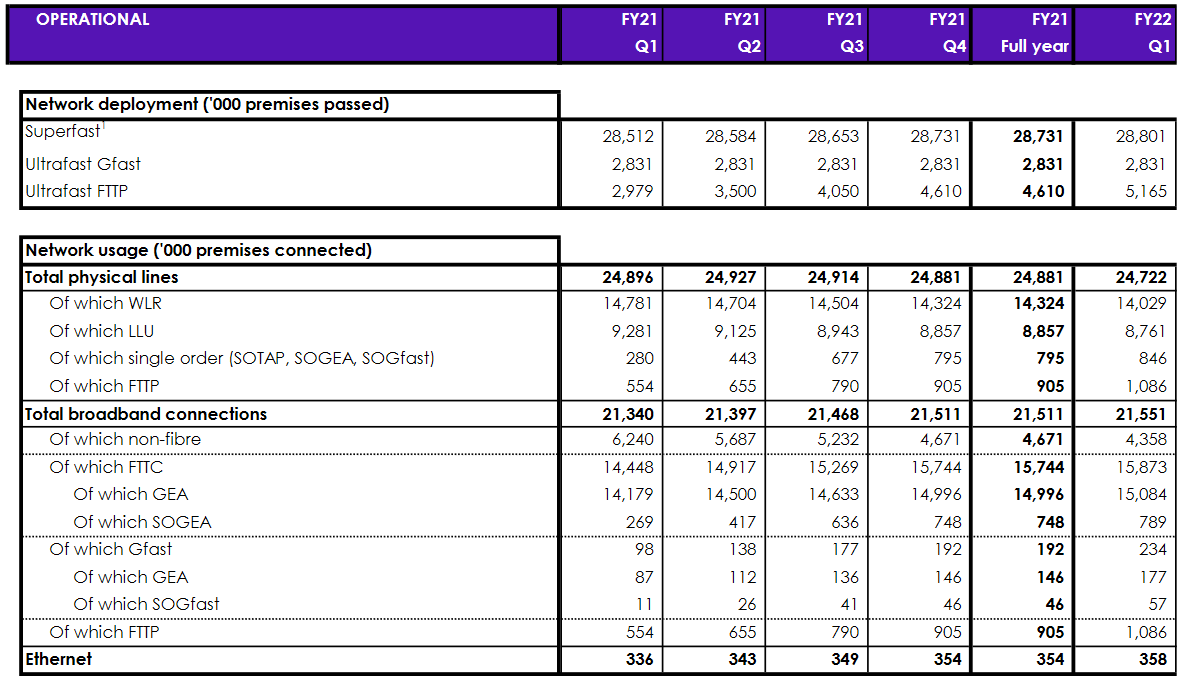

Openreach’s Network

The table below offers a breakdown of fixed line network coverage and take-up by technology on Openreach’s national UK network, which covers the totals for all ISPs that take their products combined (e.g. BT, Sky Broadband, TalkTalk, Zen Internet, Vodafone etc.).

The roll-out of full fibre lines remains the dominant one amongst the two “ultrafast” technologies, with FTTP adding +555,000 premises (down from +560K last quarter) and hybrid fibre G.fast being unchanged (G.fast deployments have long been suspended in favour of deploying more FTTP).

Advertisement

We normally expect the rapid rollout of any new technology to suppress the take-up figure, but Openreach’s FTTP still seems to be bucking this trend. The result reveals that, across all ISPs, some 1,086,000 FTTP connections have now been made (up from 905k last quarter) and that equates to a take-up of 21.03% (up from 19.6% last quarter) – this is impressive. But the operator’s plan to ramp-up their build may yet cause this to slide a bit.

Philip Jansen, CEO of BT Group, said:

“Our operational performance remained strong and our EBITDA grew during the first three months of the year, reflecting improved trading across most of our business and the positive benefits of our plans to modernise BT. Our results were overall in line with our expectations during the quarter, with good performance in the UK offsetting challenging conditions in Global’s markets.

We’re powering ahead with our network build programmes: Openreach has now built full fibre broadband to more than 5m premises with growing customer demand; EE has set out plans for 5G on demand anywhere in the UK by 2028. We’ve also reached a partnership agreement with our largest trade union, the CWU1 , allowing us to keep our modernisation plans on track.

We continue to invest in new strategic growth areas and have also today announced a strengthened strategic partnership with Microsoft that will see us accelerate co-innovation across all areas of our business, including enterprise voice and cyber security, supporting our growth strategy.

With trading conditions expected to see some improvement through the year, we have confirmed our outlook and remain confident that BT is on a path to growth.”

Otherwise, there’s not a lot to add this quarter.

Mark is a professional technology writer, IT consultant and computer engineer from Dorset (England), he also founded ISPreview in 1999 and enjoys analysing the latest telecoms and broadband developments. Find me on X (Twitter), Mastodon, Facebook, BlueSky, Threads.net and Linkedin.

« Virgin Media O2 to Upgrade Existing UK Network with Full Fibre

Apart from the Capital Deferral (£825m) beginning to disappear from the footnotes the early take-up of FTTP by existing FTTC users is worth a discussion.

If the subsidised FTTP -579k customers passed with a take up of 60-70% is extracted, then the take up by existing FTTC customers so far is a good deal less than 20% – 15-16% first pass. Is this what folk are expecting?

Care to try that again in English, please?

If the BDUK funded FTTP and take-up is subtracted from the full fibre numbers reported, it is showing early take up of full fibre by existing FTTC users is no more than 15-16%. The latter is the single most important number and will shape all other aspects of any full fibre programme.

Unrelated the only public record of £825m Capital Deferral intended to complete rural is disappearing with no explanation as to whether it was invested in rural networking or whether BT has been allowed to capitalise cash payments to LA’s instead of completing rural upgrades.

Rate at which the rollout of the city fibre in Aberdeen is going on is atrocious,3 years on still my part of city is not covered. Ended up going with BT Fttp no regrets. They are losing so many potential customers of VF and city fibre don’t step up the game.

It is good to see the FTTP coverage grow.

However, there are still many issues to be addressed.

For example, is it really necessary for certain areas to build multiple fibre infrastructures, including Openreach and others, for the same premise, while large part of this country don’t have fibre broadband at all?

Also, why doesn’t Openreach do symmetric fibre, at least for business customers? Do business customers really have to wait for an altnet to do just that?

And how will the increasing digital divide be solved?

G newton

Also, why doesn’t Openreach do symmetric fibre, at least for business customers?

that called a leased line i think

GPON isn’t symmetric, the upload is half the download. The upload offered by altnets is offered as upload is far less used so you can borrow some from others.

Whilst some announcements infer overbuild of Altnets across a town/city the actual presence in parts of the those locations may be different. All of them know they have a good run at it against OR FTTP and VM HFC in the short term. Longer term competition will be fierce with both OR and VM upgrade plans. Hence why many Alnets are going for the easier options (OR Poles) or where interest is likely to be secured against existing.

The only place I have seen direct overbuild so far is East Grinstead (OR FTTC, OR FTTP, FW Networks and phase 1 Cityfibre proposal).

OR are moving a pace but on a GPON Design probably based on cost and equipment availability. At some stage they will switch but may jump a generation to provide business in future but will stick to their dedicated high speed products. OR offer products nationally but it will not be too difficult to install later OLTs in their new centres and piggy back over the same fibres for those that need it.

OR and VM are offering assymetrical currently for cost effectiveness knowing that the use profile is assymetrical. SME profiles are also mostly assymetrical. Anyone looking for high upload should buy the product with that upload capability.

Cityfibre may say their GPON is symetrical but if you look at the Vodafone product its Average Down 900 but UPTO 900 inferring an acceptance of contention which is probably fine now while takeup is low and assumptions that few will ever use it. In some Vodafone Gigafast areas they are selling to Consumers but not currently to Businesses, they are only offered Superfast speeds. Those companies offering Business products over Cityfibre have SLAs regarding guaranteed speeds and I assume Cityfibre network settings are changed to support those SLAs. Businesses dependent on high data speed need consistent performance, resilience and therefore need to pay for it.

After all the technicalities companies still need to protect their business revenue.

The divide used to be 1 or 2 Mb to Superfast. For the next few years it will be 10Mb/no choice to Giga/Multiple Choice and not just in the remote locations. Presumably not considered part of “levelling up”.

Sorry missed out VM.

The only place I have seen direct overbuild so far is East Grinstead (OR FTTC, OR FTTP, VM FTTP, FW Networks and phase 1 Cityfibre proposal).

GPON isn’t symmetric, but XGS-PON is 10G symmetric. Openreach could choose to put in the stuff to do this now, or upgrade to it later if they wanted to.

@Billy Nomates They could and probably will, XGS PON and GPON can co-exist on the same network and usually the same OLT, I doubt Openreach are in a massive rush as it adds considerable cost for speed which only businesses, which at that size should have leased lines, would use. Despite what some on this forum say, the upload speeds on Openreach are fine.

That suggests ~ 560k FTTP connections built within 3 months.

~45k per week. Not bad for COVID times & growing.

FTTP roll-out has not accelerated in the quarter and the reported weekly orders have not increased in the quarter. The CEO said on the analyst call on 29/7/2021 – OR had been doing more rural. Perhaps BDUK will report an increase on their next update.

CEO also said that they had been building spines and can’t count the numbers until the rest of the network is complete. This is no different to any quarter. Sounds like excuses to me. To achieve 25M target by 2026 build should be accelerating to 1,000,000 homes a quarter!

I wonder how many of these premises can actually get the service, should they ask for it.

I’m supposed to be able to have FTTP service*, but despite ordering it from my ISP two months ago, I’ve only got an ONT sitting on the wall, flashing uselessly.

*A community build to boot – i.e. myself and my neighbours clubbed together to get OR to install it.

The values given are only for premises that can actually order FTTP. So everyone of the 5 million premises.

But not every ISP is offering Openreach FTTP in every location where it is available to order. And lots of ISPs don’t offer FTTP at all.

You were able to order the service, so you are counted in those figures (“properties passed”)

However, the first customer on a particular PON is the one who finds the problems, and sometimes these take a while to shake out.

interesting so if you did a community fibre partnership with openreach how have you got an ONT on your wall as that would only be there as it would be provided as part of your order with your chosen service provdiers — please advise as your statement does not make sense

Hi,

I am part of a community build with Openreach and they gave us a completion date in June.

I then ordered an upgrade through my ISP (Zen, in this case), and an ONT was installed on the second attempt. However, it is just sitting on the wall, with the PON light flashing.

It will be interesting to see when the first DSLAM’s are decommissioned.

With so many resellers onboard with effective self imposed FFTC stop sells it can’t be long now. Anyone in GFast would be a bit loopy to turn down GFast -> FTTP migration.