Credit Suisse Predict 90 Percent UK Full Fibre Coverage for 2025

A recent report from banking giant Credit Suisse has estimated that Fibre-to-the-Premises (FTTP) broadband networks will cover 90% of the UK by 2025. The country was also found to be the “most attractive market” for incremental investment in such networks, thanks to “strong build momentum and interest” in faster broadband.

At present over 30% of UK premises are believed to be covered by full fibre networks (here), yet around 65.27% can access “gigabit-capable” broadband lines (FTTP + Hybrid Fibre Coax – the latter is largely thanks to Virgin Media). Suffice to say, it’s important to caveat that the research from Credit Suisse is only concerned with FTTP and not the Government’s softer measure of gigabit-capability.

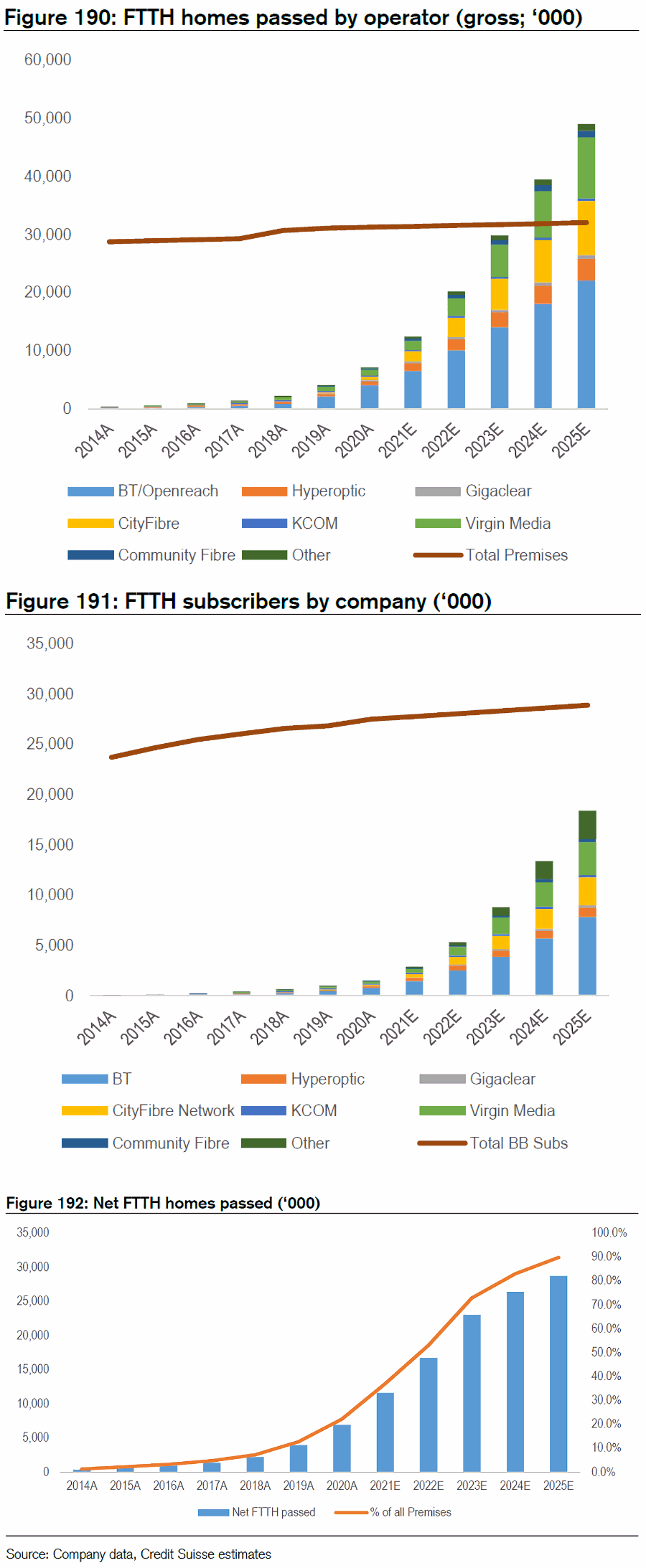

The report estimates that Openreach (BT) will end up accounting for around 69% of FTTP (FTTH) lines by 2025, while a combination of Virgin Media, CityFibre and various smaller players will add roughly another 21% net of overbuild. We should point out that the Credit Suisse forecast only extends to 2025, while Openreach’s FTTP build for 25 million premises (c.80% of the UK) aims to complete in December 2026.

Advertisement

The study also includes some predictions for KCOM, Gigaclear, CommunityFibre and Hyperoptic, but then lumps the mass of remaining Alternative Networks into the “others” category and seems to be quite conservative about how much they will achieve. Based on the recent progress of just a few of those “others” (Summary of UK Full Fibre Builds), we think their future impact may have been underestimated, but only time will tell.

The study also makes some specific premises passed predictions for several networks. For example, come 2025 it expects Openreach to have 22 million premises passed with FTTP, while Hyperoptic will be at 3.7m, Gigaclear 626,000, CityFibre 9.3m, KCOM 410,000, CommunityFibre 1.1m and Virgin Media (VMO2) on 10.5m.

The figures for most of those are not unreasonable (some are a little optimistic, but not excessively so). But Hyperoptic’s progress of late has been slow (here) and they have yet to announce any revised delivery targets for the future. Elsewhere, the level of expected overbuild is also very difficult to model without having access to the detailed forward plan of all the main players.

Advertisement

The estimate for Virgin Media is also a difficult one to judge until they’ve clarified how far their future FTTP build will actually go (i.e. beyond just the planned upgrade of HFC to XGSPON by 2028). Virgin has talked about an ambition to connect another 7 million premises over the next 4-5 years (putting them almost level with Openreach), but they have yet to turn that into a formal plan.

Speaking of Virgin Media, the report estimates that BT’s FTTP retail market was around 52% in 2020, but they expect this to fall to around 42% “given the impact of Virgin Media’s FTTH upgrade.” Certainly it seems reasonable, given the rapidly growing level of infrastructure competition, that BT’s retail share will fall, but if so it won’t just be because of Virgin.

“The UK still appears to be the most attractive market for incremental FTTH investment given strong Build Momentum and interest in superfast broadband as well as a large amount of small players offering FTTH (fragmented market) with little overbuild providing opportunity for competitive access pricing,” concluded the study.

The catch here is that the UK’s AltNet market for full fibre deployments is now quite crowded, and through 2021 we saw a rapidly rising level of overbuild between both altnets and the bigger players. In such a race there will inevitably be winners and losers, with a fair bit of consolidation expected just over the horizon. Opportunities may indeed still exist, but it’s becoming an increasingly steep hill for any new entrants to climb.

Advertisement

One other uncertainty is the impact of the Government’s £5bn Project Gigabit programme, which won’t really be known until we start to see how successful they’ve been with their first few procurement waves. In any case, the first physical builds under that project won’t really start until late 2022 or 2023, and it’ll then take time to ramp-up after that.

NOTE: This report was sent to us privately, and we’ve yet to find a public link for it.

Mark is a professional technology writer, IT consultant and computer engineer from Dorset (England), he also founded ISPreview in 1999 and enjoys analysing the latest telecoms and broadband developments. Find me on X (Twitter), Mastodon, Facebook, BlueSky, Threads.net and Linkedin.

« BT Begin OpenRAN Trial in Hull UK to Boost Mobile Broadband

BT Set to Create 600 New UK Apprenticeship and Graduate Jobs »

May be 2050

Because Credit Suisse know technology so well eh? I’d be surprised to see real fibre in my road before 2050-60

Just as well the UK can get to 99.99% coverage without building in your street, Lugz.

The market conditions for investment in FTTP/4&G created by the Conservative government over the last 10 years have been a huge success, it has to be said. Credit where credit is due.

I see what you did there William.

I’ve got to be honest I’ll believe it when I see it. While cities are well served (with multiple providers fighting) and most large towns have one provider rolling out now there are still many small towns and villages with nothing. With return on investment being so long people in these areas are basically waiting on the Openreach lottery or the vague hope an altnet gets enough expressions of interest the actually roll out as promised (and surveys showing the job isn’t too hard). I won’t even try and classify true rural properties chances (USO, gov vouchers etc). I can definitely see the 60~70% coverage being hit easily (With probably 40%+ overbuild by 2 or more networks). Its the next 30~40% that will be increasingly slow as all the easy profitable targets have been plucked (or double/triple plucked).

I hope Credit Suisse did better research on this than they did for Archegos($5.5 billion loss), Greensill($2.3 billion loss) and their new chairman (multiple Covid quarantine violations).

Our great leaders setting an example eh….

With BT phasing out the old analog lines that will drive up the roll out of FTTP

They have to reach 75% able to access FTTP before they put a stop on copper line orders, so not much of a drive there

PIA

If an Alt Net provider encounters a blockage and clears it does Open Reach contribute towards the cost of clearing it ?

No.

Yes

I’ve been wondering the same myself. My town has lots of 70s ducting (Several 70s estates). Those have to be in a pretty bad shape now after 50 years. I do wonder if this is why openreach have skipped us every time as even the local villages that are getting picked will have better investment returns as they are all simple pole deployments. I wonder if Openreach are waiting for an altnet to foot the bill first?

The Alt-Net has to pay a few hundred pounds. BT may statre they “contribute” but that’s just a number on the quote, not actual cash.

Not without radical changes to the current fiasco. The advantages with fibre technology mean less maintenance , faster speeds, and hence the potential for enhanced service such as hdtv, off site backups, holographic communications etc. Not sure when Dankshire will be blessed with such technology. Perhaps as the ex PM said we will find gigabit in the hedgerows!!

I’m astonished Openreach haven’t abandoned their current rollouts to prioritise Dankshire but given I guess no-one else has shown any interest either the competitive pressure is low.

Same story as a large proportion of the country outside of urban areas.

Get an alternative network in and Openreach will follow. If that isn’t happening perhaps Dankshire isn’t such a great prospect commercially and needs taxpayer subsidy.