Interview – Openreach on UK FTTP Rollout, Competition and Future Plans

Yesterday Openreach (BT) announced the milestone of having covered 2 million UK premises with Fibre-to-the-Premises (FTTP) broadband technology (here). As part of that we’ve conducted an exclusive interview with the operator’s MD for Fibre and Network Delivery, Kevin Murphy, to talk about their future fibre plans.

As most people know, Openreach currently aim to cover 4 million premises with their Gigabit-capable “full fibre” network by March 2021 and after that they hold an ambition to reach 15 million by around c.2025, as well as an even longer-term aspiration to reach the “majority” of UK homes and businesses.

Suffice to say that we wanted to know more about how all of this would be achieved, as well as what sort of progress we should expect to be seeing over the coming years, when public subsidy might be required to go further, how Openreach is responding to rival networks in the same space (overbuild), the future of G.fast and various other things.

Advertisement

Mercifully Kevin Murphy has been kind enough to help answer some of our questions.

The Interview

Question 1. Firstly, congratulations on reaching the 2 million FTTP premises passed milestone. Openreach has come quite a long way since the official start of your “Fibre First” programme in early 2018 and the rate of build is continuing to ramp-up.

At present we understand that you’re building at an average rate of around 24,000 premises per week and the latest BT Group results predicted that you might even exit 2019/20 with a stronger run rate of 30,000 per week.

Assuming the build continues toward the 15 million ambition by c.2025, then what sort of weekly peak do you predict that Openreach might be able to achieve in a few years’ time?

Advertisement

ANSWER:

We’re really pleased with the progress that our engineering teams are making from virtually a standing start two years ago.

Reaching two million homes and businesses means we’re on track to meet our four million target by the end of March 2021, and it’s helped us push full fibre coverage for all networks up to around 10 per cent of the UK. There’s obviously still a long way to go, but that figure’s important because we’ve always said we can’t upgrade the country alone.

Currently we’re building full fibre to another home or business every 26 seconds – or around 1.2m a year. Our weekly run rate of 23,000 is an average across the last quarter but ultimately, if the Government and Ofcom put the right enablers in place, we’re confident that we could get to a build rate of around three million premises per year.

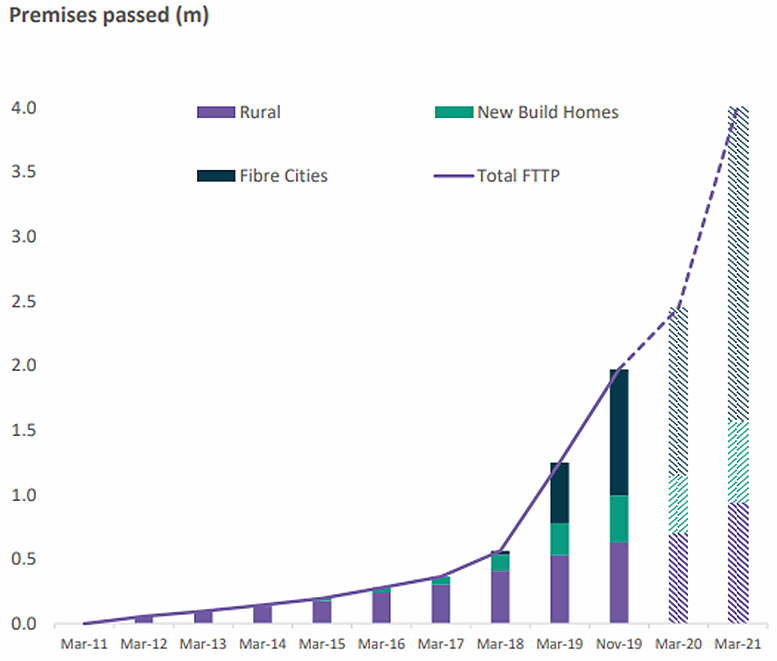

Question 2. Can you offer a rough breakdown of where all these FTTP premises are (i.e. those built so far)? Such as in terms of how many are in publicly funded BDUK areas, how many in cities/towns, how many are via new build home developments and what is the split between businesses and homes etc.?

ANSWER:

First it’s important to say we’ve never been just a city fibre broadband builder. We’re committed to delivering full fibre to the UK’s rural communities and we believe other network builders should be investing in rural areas too.

A quarter of our current full fibre footprint is in what Ofcom would class as rural (Market 3) areas and this kind of proportion could broadly stay the same.

Looking at the “FTTP Fibre First Towns, Cities and Boroughs Build Programme”, which excludes BDUK areas, new sites and other smaller scale build, since we began back in February 2018, we’ve massively accelerated our urban build, and back in October we laid out our roadmap within this programme to four million by March 2021 – encompassing 103 towns, cities and boroughs. Physical building work is already underway in three quarters of those locations.

The chart below gives a rough idea of the split across our various major build programmes.

As for the split between businesses and homes – that’s always a tough one to define accurately given the millions of small businesses and sole traders in the UK which are located within homes.

Question 3. Openreach has previously hinted that, provided the conditions are right, it might even be possible to go beyond 15 million premises and reach the “majority” of the UK. We recall that the commercial FTTC rollout stopped in 2014 at around 66% of the UK but that obviously required less civil engineering (cheaper).

Assuming a purely commercial deployment, can you offer any indication of how far beyond 15 million it might be possible to go after 2025 or would anything beyond this point require public subsidy? Where do you draw the line?

ANSWER:

We think that with the right regulatory framework, up to 90% of the UK could be attractive for full fibre investment. Right now, it’s costing us towards the lower end of £300-£400 per premises to deliver full fibre, and we’re increasingly confident that we can build to around half of UK premises within that range.

We’re also conducting trials to reduce our build costs in rural areas – using a range of new tools and techniques that we hope will help break down the cost barriers to commercial investment even further.

Question 4. Speaking of 15 million premises, Openreach expects to pass around 50% of UK premises within the current range of costs (i.e. £300 – £400 per premises passed). A rough estimate suggests this means it will cost you a little over £5bn to deliver on the first 15 million.

Advertisement

However, as an operator you’ve also previously suggested that tackling the final 10% of premises could push build costs up to £4,000 per premises, while Ofcom has estimated a much lower capex figure of up to £2,500 per premises (here).

Why the huge difference in estimates, what do you think Ofcom has got right or wrong in their figures? Likewise what sort of average build costs might we expect across the final 20%, rather than 10%, of premises.

ANSWER:

It’s very difficult to put an average build cost figure on the final 10%, but we know from experience that some homes cost tens, or even hundreds of thousands of pounds to connect – more than the cost of the house itself in many cases.

Over the last few years we’ve had lots of first-hand experience delivering full fibre to some of the most remote communities in the UK – everywhere from the Outer Hebrides to Isles of Scilly – and through some of the most challenging terrains. We know granite isn’t cheap or easy to dig through.

We’ve also scouted the world for the very best and latest tools and techniques to reach remote locations and our ongoing rural trials are giving us an opportunity to test these at scale and to get a better understanding on costs in challenging areas.

Question 5. At present Openreach and other operators are benefiting from a 5 year holiday on business rates for new fibre lines, which rises to 10 years in Scotland. However operators often create payback models for full fibre that can run to 15-20 years, which conflicts with the limited 5 year relief.

Have you been given any indication whether the UK Government might be willing to extend the current 5 year relief on business rates for new fibre (assuming you’d want this, although we can’t see why you wouldn’t)?

ANSWER:

Like us, the Government is extremely ambitious about full fibre broadband and they’ve seen from the research we commissioned that it can deliver a huge potential windfall for the UK – in terms of productivity, the UK’s workforce and the environment. So there’s every reason to believe they see the benefits of tackling this issue which affects all network builders.

We and others in the industry have been making the case consistently over the past year. Progress hasn’t been as quick as we’d have hoped on this and some of the other key enablers to investment, but with the bolder ambitions from the new Government we have every reason to believe that they’re listening and understanding the importance of making this change. We continue to believe there is a strong case for exempting full fibre from the business rates system in order to support investment from across the sector.

Question 6. Speaking of incentives for building FTTP, the Government’s current Gigabit Broadband Voucher scheme is about to run out of money (excluding the similar Rural Gigabit Connectivity Scheme). Do you think the gigabit voucher scheme has been a success and would you like to see it being extended with more funding?

ANSWER:

The fact that it’s about run out of funds is a pretty good indication of how successful the scheme’s been.

From an Openreach perspective, we’ve worked with more than 200 communities that have used vouchers totalling around £4.5 million through our Community Fibre Partnership programme. That’s helped us deliver full fibre broadband to more than 6,800 homes and businesses that weren’t in anyone’s upgrade plans – so it’s been a huge success.

More than 930 communities have now signed up to partner with us on the programme, and I’m convinced that hundreds more would follow suit if access to vouchers continued.

Please click over to page 2 below in order to continue reading this interview..

Mark is a professional technology writer, IT consultant and computer engineer from Dorset (England), he also founded ISPreview in 1999 and enjoys analysing the latest telecoms and broadband developments. Find me on X (Twitter), Mastodon, Facebook, BlueSky, Threads.net and Linkedin.

« Openreach’s FTTP Broadband Build Hits 2 Million UK Premises

Openreach Blocking Copper Broadband at UK New Build Sites »

Comments are closed